A Canadian investor earning $70,000 decides to save for the future. One option offers a tax deduction today. The other promises tax-free withdrawals later. Choosing between them often comes down to understanding taxes, income levels, and long-term goals. That’s where the question tfsa vs rrsp which is better becomes critical.

Both accounts help Canadians grow investments efficiently, but they work differently. A Tax-Free Savings Account focuses on flexibility and tax-free withdrawals, while a Registered Retirement Savings Plan emphasizes tax deductions and retirement planning. This guide explains the differences, shows real examples, and helps you decide which account fits your financial situation best.

Table of Contents

TFSA vs RRSP Which Is Better? A Complete Canadian Guide to Choosing the Right Account

Understanding the difference between these two accounts helps Canadians build smarter long-term financial plans. Both are registered investment accounts recognized by the Canada Revenue Agency (CRA), but they solve different financial problems.

One focuses on flexibility and tax-free withdrawals. The other focuses on reducing taxes today while saving for retirement. The best choice depends on income level, retirement plans, and how soon you might need the money.

Understanding TFSA and RRSP Basics

Before comparing strategies, it helps to understand what each account actually does. The rules may look simple on the surface, but the tax treatment makes a big difference over time.

What Is a Tax-Free Savings Account (TFSA)?

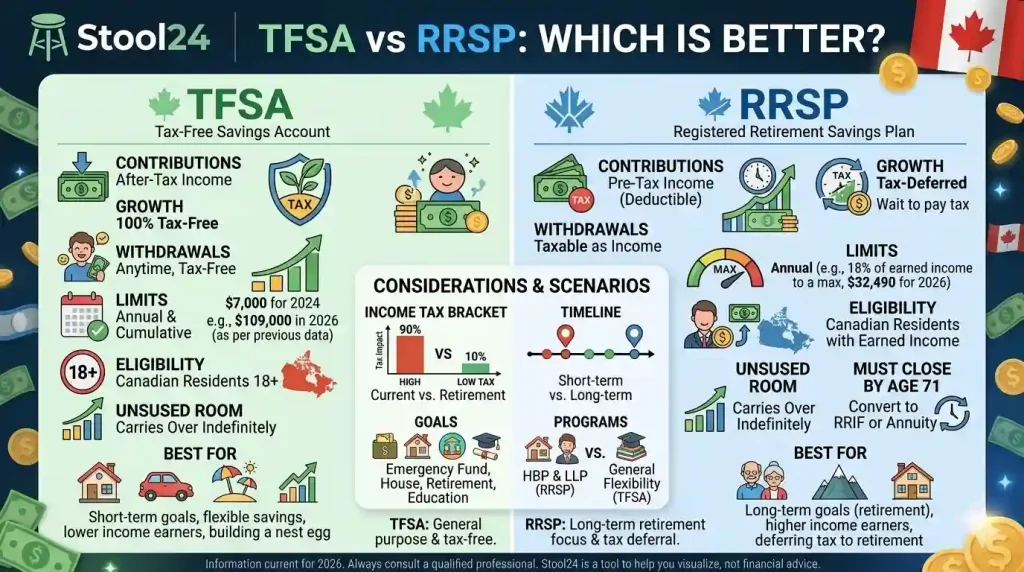

A TFSA allows Canadians to invest money and withdraw it later without paying tax on the gains. Contributions are made with after-tax dollars, meaning you don’t receive a tax deduction when depositing money.

The benefit appears later. Investment growth and withdrawals are completely tax-free, which makes the account ideal for flexible savings goals like emergencies, travel, or retirement.

You can review current limits and rules in this guide about TFSA contribution limits in Canada.

What Is a Registered Retirement Savings Plan (RRSP)?

An RRSP works differently. Contributions reduce your taxable income for the year. If someone earning $80,000 contributes $10,000 to an RRSP, their taxable income drops to $70,000.

Investments grow tax-deferred inside the account. However, withdrawals are taxed later as income, typically during retirement when the tax rate may be lower.

Key Purpose of Each Account in Canadian Financial Planning

Financial planners often view the accounts this way:

- TFSA: flexible savings and tax-free withdrawals

- RRSP: retirement savings with tax reduction

- Both: long-term investment growth

According to the Government of Canada financial guidance, registered accounts help Canadians reduce taxes and build retirement security.

TFSA vs RRSP Which Is Better: Key Differences Explained

The best way to understand the difference is to compare the core features side by side.

This table shows the key differences between TFSA and RRSP accounts.

| Feature | TFSA | RRSP |

|---|---|---|

| Contribution tax treatment | No tax deduction | Tax deductible |

| Withdrawal tax | Tax-free | Taxed as income |

| Contribution limits | Fixed annual limit | 18% of earned income |

| Withdrawal flexibility | Flexible anytime | Restricted before retirement |

| Best use | Flexible savings | Retirement tax planning |

Tax Treatment of Contributions and Withdrawals

The main difference is taxation timing. TFSA contributions are made with after-tax income, but withdrawals remain tax-free.

RRSP contributions reduce taxes today but withdrawals later are taxed as income. That difference is why choosing between the two depends heavily on your current tax bracket.

Contribution Limits and Carry-Forward Rules

TFSA limits increase periodically. Unused room carries forward forever. RRSP contribution room also accumulates but depends on income each year.

Both accounts penalize over-contributions, so tracking limits matters.

Withdrawal Flexibility and Penalties

TFSA withdrawals are simple. Take money out anytime, and the contribution room returns the following year.

RRSP withdrawals can trigger tax withholding and permanently reduce contribution room unless they fall under special programs.

Age Limits and Account Rules

RRSP contributions generally stop at age 71. At that point the account converts into a RRIF. TFSA accounts have no age limit and can remain active indefinitely.

TFSA vs RRSP Which Is Better for Different Income Levels

Income level often determines which account offers the biggest tax advantage.

Low Income Earners (Under $50,000)

For lower income Canadians, the tax deduction from an RRSP may not provide large savings. In many cases, using a TFSA first offers better flexibility.

Withdrawals later remain tax-free and don’t affect government benefits like the Guaranteed Income Supplement.

Middle Income Canadians ($50k–$100k)

This income range often benefits from using both accounts strategically. Some savings go into RRSP for tax reduction, while additional savings grow inside a TFSA.

This balanced approach spreads tax risk across future years.

High Income Professionals ($100k+)

High-income earners often receive the greatest benefit from RRSP deductions. A large contribution can significantly reduce income tax owed in a given year.

According to analysis by NerdWallet Canada financial research, higher tax brackets increase the value of RRSP deductions.

Example Scenario: $70,000 Salary Investment Strategy

Imagine someone earning $70,000 who invests $6,000 each year.

They could contribute $3,000 to an RRSP to lower taxes and place the remaining $3,000 in a TFSA for flexible withdrawals.

This strategy spreads both tax benefits and future flexibility.

Quick comparison:

Income scenario and recommended strategy.

| Income Level | Recommended Strategy |

|---|---|

| $40,000 | Focus on TFSA |

| $70,000 | Mix TFSA and RRSP |

| $120,000 | Prioritize RRSP |

When TFSA Is Better Than RRSP

In several situations the TFSA provides a clear advantage.

Saving for Short-Term Goals

If you may need money within five years, TFSA withdrawals remain tax-free and flexible.

This makes the account suitable for emergency funds, travel savings, or major purchases.

Avoiding OAS Clawbacks in Retirement

TFSA withdrawals do not count as taxable income. That means they do not affect Old Age Security benefit calculations.

This detail becomes important for retirees managing multiple income sources.

Young Investors With Lower Tax Brackets

Younger Canadians often earn lower incomes early in their careers. Using a TFSA during those years can make more sense than claiming small RRSP deductions.

Emergency Fund and Flexible Savings

Unexpected expenses happen. Having accessible savings without tax consequences offers peace of mind.

A TFSA works well as both an investment account and an emergency fund.

When RRSP Is Better Than TFSA

While the TFSA is flexible, the RRSP shines in specific financial situations.

Reducing Taxes in High Income Years

When income jumps into a higher tax bracket, RRSP contributions provide immediate tax relief. This benefit can reduce the total tax owed for the year.

Employer RRSP Matching Benefits

Some employers match RRSP contributions. That essentially provides free investment money.

Ignoring employer matching means leaving guaranteed returns on the table.

Retirement Income Tax Strategy

Many retirees earn less income after leaving the workforce. If RRSP withdrawals occur in a lower tax bracket, the strategy becomes tax-efficient.

Using RRSP for Home Buyers Plan

The Home Buyers’ Plan allows first-time buyers to withdraw funds from an RRSP without immediate tax, provided the money is repaid later.

You can learn about withdrawal timing in this guide about when to withdraw RRSP funds.

Smart Strategy: Using Both TFSA and RRSP Together

For many Canadians, the real answer to tfsa vs rrsp which is better is actually both.

The TFSA-First Strategy

Some investors begin by maximizing TFSA contributions for flexibility and tax-free growth.

Once that room is filled, they contribute additional savings to an RRSP.

The RRSP-First Strategy

Higher-income professionals often reverse the order. They prioritize RRSP contributions to reduce taxes today.

Tax refunds generated by the RRSP can then be reinvested into a TFSA.

Balanced Contribution Strategy

A balanced approach spreads contributions across both accounts each year.

This protects against future tax uncertainty while maintaining flexible savings.

Sample Investment Allocation Plan

A common strategy looks like this:

- Emergency savings inside a TFSA

- Retirement contributions to RRSP

- Additional investment growth inside TFSA

Financial planning tools can help estimate long-term growth.

A quick projection using a calculator can reveal how small annual TFSA contributions grow over decades.

Try the TFSA Growth Calculator

Common Mistakes Canadians Make With TFSA and RRSP

Even experienced investors sometimes misuse these accounts. Avoiding a few common mistakes can significantly improve long-term results.

Over-contributing and CRA Penalties

Exceeding contribution limits triggers monthly penalties from the Canada Revenue Agency. Tracking available room prevents unnecessary fees.

Ignoring Tax Bracket Strategy

Contributing to an RRSP when income is very low may waste valuable deduction potential.

Withdrawing RRSP Too Early

Early withdrawals trigger taxes and permanently remove contribution room. This can weaken long-term retirement savings.

Not Reinvesting RRSP Tax Refunds

Many Canadians spend their RRSP tax refund instead of reinvesting it.

Reinvesting that refund into a TFSA or RRSP significantly boosts long-term returns.

Smart investors often combine tools such as the Tax Toolkit financial planning resources to compare tax scenarios before making decisions.

FAQS For tfsa vs rrsp which is better

Is TFSA better than RRSP for retirement in Canada?

A TFSA can be better for retirement if you expect to stay in a similar or higher tax bracket later in life. Withdrawals are completely tax-free and do not affect government benefits like Old Age Security. However, RRSPs can be more powerful if your current income tax rate is significantly higher than your expected retirement rate.

Should I max out my TFSA before contributing to an RRSP?

Many financial planners suggest maxing out a TFSA first if your income is relatively low or moderate. This approach keeps your savings flexible while allowing tax-free growth. Once income increases, contributing to an RRSP for tax deductions can become more beneficial.

Can Canadians have both a TFSA and an RRSP at the same time?

Yes, Canadians can contribute to both accounts in the same year as long as they stay within the contribution limits. Each account serves a different purpose—TFSA offers tax-free withdrawals while RRSP reduces taxable income. Using both accounts together is often the most balanced long-term strategy.

At what income level is an RRSP usually better than a TFSA?

An RRSP often becomes more valuable once income reaches higher tax brackets, typically around $80,000 or more depending on the province. At that level, the tax deduction can significantly reduce annual taxes owed. Lower-income earners may benefit more from the flexibility of a TFSA.

What happens if you withdraw money from an RRSP early?

Early RRSP withdrawals are taxed as income in the year you take the money out, and withholding tax may apply immediately. The withdrawn amount also permanently reduces your contribution room. This is why RRSPs are usually considered long-term retirement accounts.

Does a TFSA affect government benefits in Canada?

No, TFSA withdrawals are not counted as taxable income and generally do not impact federal benefits. Programs such as Old Age Security and the Guaranteed Income Supplement remain unaffected. This makes the TFSA especially useful for retirement income planning.

Can I move money from a TFSA to an RRSP?

Yes, you can withdraw money from a TFSA and contribute it to an RRSP, but the contribution will count toward your RRSP limit. The TFSA contribution room will be restored the following calendar year. Some investors use this strategy to shift savings into RRSPs during higher-income years.

Quick Summary

The debate around tfsa vs rrsp which is better depends largely on income level, tax strategy, and personal financial goals.

- TFSA offers flexibility and tax-free withdrawals.

- RRSP provides immediate tax deductions and retirement planning advantages.

- Lower income Canadians often benefit from TFSA first.

- Higher income earners typically gain more from RRSP deductions.

- Using both accounts together creates the most balanced long-term strategy.

With thoughtful planning, these accounts can work together to reduce taxes, grow investments, and build a stronger financial future.