A Canadian worker earning $75,000 might assume their RRSP should stay untouched until retirement. Yet tax timing often matters more than age. Knowing when to withdraw RRSP funds can reduce taxes, smooth retirement income, and even protect government benefits.

In Canada, RRSP withdrawals are fully taxable and can push you into a higher tax bracket if done poorly. The right strategy depends on income level, retirement timing, and long-term tax planning. This guide explains how RRSP withdrawals work, when early withdrawals make sense, and how Canadians can reduce tax impact with smarter timing strategies.

Table of Contents

When to Withdraw RRSP: Best Timing Strategies to Reduce Taxes in Canada

Understanding the right time to withdraw from your RRSP is not just about retirement age. It’s about tax efficiency. In Canada, withdrawals can occur anytime, but every dollar is treated as taxable income. The challenge is finding the timing that keeps taxes lower while preserving retirement savings.

Financial planners often recommend thinking about withdrawals years before retirement. By spreading withdrawals across low-income years, many Canadians reduce total lifetime tax payments.

Understanding RRSP Withdrawals in Canada

Before deciding when to withdraw RRSP savings, it helps to understand the rules. Registered Retirement Savings Plans were designed to defer taxes. Contributions reduce taxable income today, while withdrawals are taxed later.

This tax deferral can be powerful when income is lower in retirement.

What an RRSP Is and How Withdrawals Work

An RRSP allows Canadians to invest pre-tax income for retirement. Contributions reduce current taxable income, which is why many workers use RRSPs during high-earning years.

However, when money is withdrawn, the amount is added to your annual income and taxed at your marginal rate. The Canada Revenue Agency (CRA) treats these withdrawals just like employment income.

Can You Withdraw from an RRSP Anytime?

Yes, withdrawals can occur anytime. There are no penalties like those found in some international retirement plans. However, two important consequences apply:

- The withdrawn amount becomes taxable income

- Your RRSP contribution room is not restored

Because contribution room is permanently lost, early withdrawals should be planned carefully.

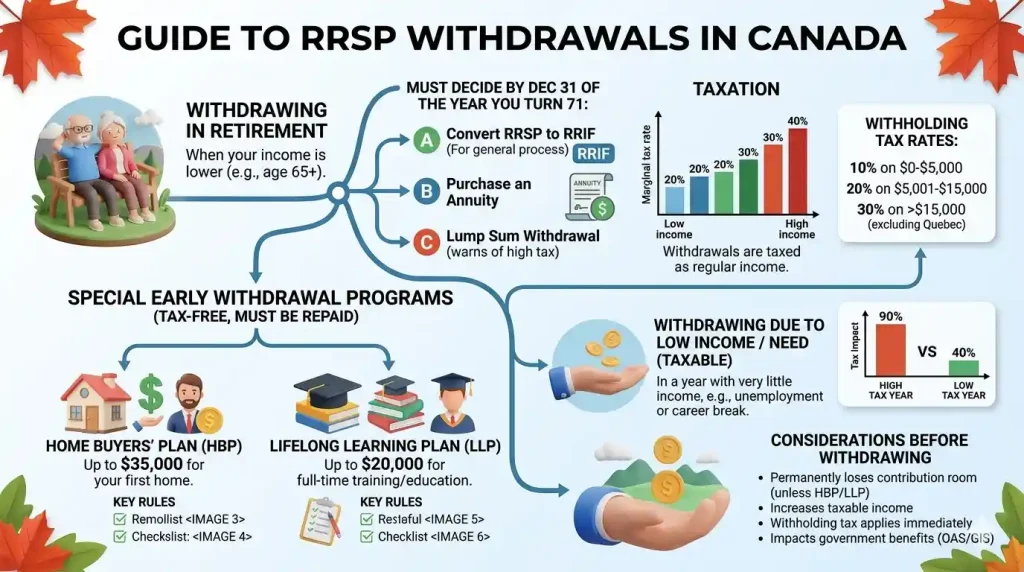

RRSP Maturity Rules (Age 71 Requirement)

Canadian rules require RRSP accounts to mature by December 31 of the year you turn 71. At that point, the account must be converted into a retirement income option such as a Registered Retirement Income Fund (RRIF) or an annuity.

After conversion, minimum withdrawals must begin each year.

RRSP vs RRIF: What Happens After 71

A RRIF functions similarly to an RRSP but requires mandatory withdrawals. The government sets minimum withdrawal percentages based on age. According to the Government of Canada, the minimum RRIF withdrawal at age 72 is roughly 5.4% of the account balance.

This is why some retirees start strategic withdrawals earlier — to control taxes before mandatory withdrawals begin.

When to Withdraw RRSP: Key Timing Strategies

Determining when to withdraw RRSP funds often depends on income levels and retirement timing. Many Canadians benefit from withdrawing during years when their income temporarily drops.

Smart timing can significantly reduce the total tax paid over decades.

When to Withdraw RRSP During Low-Income Years

If income drops because of a job transition, parental leave, or early retirement, that year may offer an ideal window for withdrawals.

For example, someone earning $40,000 instead of $80,000 may fall into a lower tax bracket. Taking a moderate withdrawal during this period can result in significantly lower taxes.

Withdrawing After Retirement

Most Canadians begin withdrawals after retiring and before age 71. This period often provides flexibility because employment income has stopped, but government benefits like CPP or OAS may not have started yet.

Careful planning during this phase can prevent large taxable withdrawals later.

Strategic Early Withdrawal Planning

Some financial planners suggest early withdrawals in small amounts to reduce future RRIF withdrawals. This approach is often called “income smoothing.”

Instead of facing large withdrawals later in life, income is spread over more years, keeping tax rates lower.

Partial vs Lump-Sum Withdrawals

Taking one large withdrawal can push income into a higher bracket. Spreading withdrawals across several years usually results in less tax overall.

Even a $20,000 withdrawal divided over four years can significantly reduce taxes compared to a single lump sum.

RRSP Withdrawal Tax in Canada

When money is withdrawn, financial institutions apply withholding tax. This is not the final tax owed; it is simply a prepayment toward your annual tax bill.

The table below shows the standard withholding tax rates applied to RRSP withdrawals in most Canadian provinces.

This table shows typical RRSP withholding tax rates applied to withdrawals.

| Withdrawal Amount | Withholding Tax Rate |

|---|---|

| $0 – $5,000 | 10% |

| $5,001 – $15,000 | 20% |

| $15,000+ | 30% |

These rates are applied by banks or investment providers when processing the withdrawal.

Your final tax bill may be higher or lower depending on total annual income.

How Withdrawals Affect Your Marginal Tax Rate

Because RRSP withdrawals are added to taxable income, they may push you into a higher bracket.

For instance, a retiree earning $45,000 who withdraws $25,000 will now report $70,000 in taxable income.

That jump can increase the tax owed on the withdrawal.

Example: Tax Impact of a $20,000 Withdrawal

Imagine withdrawing $20,000 from an RRSP. The financial institution may withhold $6,000 at a 30% rate. However, your final tax rate might be lower depending on your total income.

That’s why planning withdrawals carefully can prevent unnecessary tax payments.

Situations When Early RRSP Withdrawals Make Sense

Despite the tax impact, there are legitimate situations where early withdrawals make sense.

Canadian tax policy includes programs designed to allow temporary withdrawals without immediate taxation.

Home Buyers’ Plan (HBP)

The Home Buyers’ Plan allows first-time buyers to withdraw up to $35,000 from their RRSP to purchase a home.

Funds must be repaid over 15 years to avoid taxation.

Lifelong Learning Plan (LLP)

The LLP allows withdrawals to fund education or training. Participants can withdraw up to $20,000 total for qualifying programs.

Repayment typically begins five years after the withdrawal.

Unexpected Financial Emergencies

Sometimes withdrawals are unavoidable. Job loss, medical costs, or family emergencies can force access to retirement savings.

In those cases, understanding the tax consequences helps prevent unpleasant surprises at tax time.

RRSP Withdrawal Strategies to Reduce Taxes

Tax planning becomes especially important as retirement approaches.

Several strategies can help Canadians minimize taxes while withdrawing RRSP funds.

The RRSP Meltdown Strategy

This approach involves gradually withdrawing RRSP funds while replacing them with tax-deductible investments or using leverage strategies. The goal is to reduce future RRIF balances and taxable withdrawals.

It’s usually used by high-income retirees working with financial advisors.

Using RRSP Withdrawals Before CPP and OAS

Some retirees delay government benefits and instead withdraw RRSP funds first. This reduces account size before mandatory RRIF withdrawals begin.

It can also prevent Old Age Security (OAS) clawbacks later in retirement.

Balancing RRSP and TFSA Withdrawals

Tax-Free Savings Accounts provide tax-free withdrawals, making them a valuable complement to RRSPs.

This table compares RRSP and TFSA withdrawals.

| Feature | RRSP | TFSA |

|---|---|---|

| Tax on withdrawal | Yes | No |

| Contribution room restored | No | Yes |

| Impact on benefits | Possible | None |

Balancing both accounts often produces better tax outcomes over time.

Spreading Withdrawals Across Multiple Years

Instead of withdrawing $100,000 in one year, spreading withdrawals over five years can significantly reduce taxes.

This approach keeps income within lower brackets and improves long-term tax efficiency.

Planning tools can help estimate the tax impact.

A quick estimate using a retirement calculator can reveal how different withdrawal amounts affect taxable income.

Use the RRSP Calculator to Estimate Your Withdrawal Taxes

Common RRSP Withdrawal Mistakes to Avoid

Even experienced investors sometimes make costly withdrawal mistakes. Avoiding a few common errors can protect retirement savings.

Withdrawing During Peak Income Years

If you are earning your highest salary, withdrawing RRSP funds can push income into the highest tax bracket.

In most cases, waiting until retirement or a lower-income year produces better results.

Taking Large Lump-Sum Withdrawals

Large withdrawals often trigger higher withholding tax and push total income into higher brackets.

Breaking withdrawals into smaller annual amounts is usually more tax efficient.

Ignoring Government Benefit Clawbacks

High taxable income during retirement can reduce benefits such as Old Age Security. According to the Government of Canada, OAS begins clawbacks once income exceeds certain thresholds.

Strategic withdrawals can help avoid these reductions.

Not Planning for Retirement Income

RRSP withdrawals should be part of a broader retirement income strategy. CPP, OAS, and personal savings all play roles.

Using tax tools and planning resources helps Canadians optimize these decisions.

Many Canadians also explore tax-reduction strategies explained in the RRSP income tax reduction guide.

Additional calculators and planning resources are available inside the Tax Toolkit.

Example Scenarios: When It Makes Sense to Withdraw RRSP

Real-life situations often illustrate RRSP strategy better than theory.

Scenario 1: Early Retirement Strategy

A 60-year-old retires early with minimal income for five years before CPP begins. Withdrawing moderate RRSP amounts during those years can reduce taxes and prevent large RRIF withdrawals later.

Scenario 2: Low Income Year Tax Optimization

A worker returning to school temporarily earns only $30,000. Taking a $10,000 withdrawal during that year could fall within a lower tax bracket.

Scenario 3: First-Time Home Purchase

A buyer withdraws $35,000 under the Home Buyers’ Plan to fund a down payment. Because the withdrawal is repaid over time, it avoids immediate taxation.

FAQS For when to withdraw rrsp

When should you withdraw from an RRSP in Canada?

The best time to withdraw from an RRSP is usually during years when your income is lower. This keeps your marginal tax rate lower and reduces the total tax paid on the withdrawal. Many Canadians start partial withdrawals after retirement but before mandatory RRIF withdrawals begin.

Can you withdraw money from an RRSP before retirement?

Yes, you can withdraw RRSP funds at any time in Canada. However, the withdrawal is treated as taxable income and may increase your tax bracket for that year. Early withdrawals should be planned carefully to avoid unnecessary taxes.

How much tax do you pay on RRSP withdrawals?

Financial institutions apply withholding tax when you withdraw money from an RRSP. Typically, the rate ranges from 10% to 30% depending on the withdrawal amount. Your final tax amount may differ because the withdrawal is added to your total taxable income for the year.

Is it better to withdraw RRSP before age 71?

In many cases, withdrawing some RRSP funds before age 71 can help reduce taxes later. This strategy lowers the balance before it converts to a RRIF, which has mandatory withdrawals. Smaller withdrawals over several years often result in better tax efficiency.

Can RRSP withdrawals affect government benefits in Canada?

Yes, RRSP withdrawals increase your taxable income and may affect income-tested benefits. Higher income can reduce benefits such as Old Age Security or the Guaranteed Income Supplement. Planning withdrawals carefully helps avoid unexpected clawbacks.

Are there tax-free RRSP withdrawals in Canada?

Certain programs allow temporary tax-free withdrawals from an RRSP. The Home Buyers’ Plan and the Lifelong Learning Plan allow eligible Canadians to withdraw funds without immediate taxation. The withdrawn amount must be repaid to the RRSP over time.

Should you withdraw from RRSP or TFSA first?

This depends on your retirement income and tax situation. Many advisors recommend using RRSP withdrawals strategically in lower-income years while keeping TFSA funds for tax-free flexibility. Combining both accounts can help reduce lifetime taxes.

Quick Summary

The best answer to when to withdraw RRSP funds depends on income, retirement timing, and long-term tax planning.

- Withdraw during low-income years whenever possible

- Avoid large lump-sum withdrawals

- Plan withdrawals before mandatory RRIF rules begin

- Balance RRSP and TFSA withdrawals

- Consider government benefit impacts

With thoughtful planning, RRSP withdrawals can support retirement while minimizing taxes across decades.