A borrower in Toronto wants $15,000 for a home renovation. Another person in Calgary needs money to cover an unexpected medical bill. Both are looking for financing, but the loan type they choose can dramatically affect interest rates, approval chances, and financial risk. That’s where understanding unsecured vs secured loan Canada becomes essential.

In simple terms, secured loans require collateral, while unsecured loans rely mostly on your creditworthiness. But the real differences go deeper—interest costs, approval requirements, and even what happens if you miss payments. This guide explains how these loan types work in Canada, when each option makes sense, and how to choose the right one for your situation.

Table of Contents

Unsecured vs Secured Loan Canada: Key Differences, Pros, and Which Is Better

Choosing between secured and unsecured borrowing can shape your financial future. Canadian lenders evaluate risk carefully, and the structure of your loan determines how much you can borrow and how much it will cost over time.

Understanding these differences helps borrowers avoid expensive mistakes and select the most practical loan for their needs.

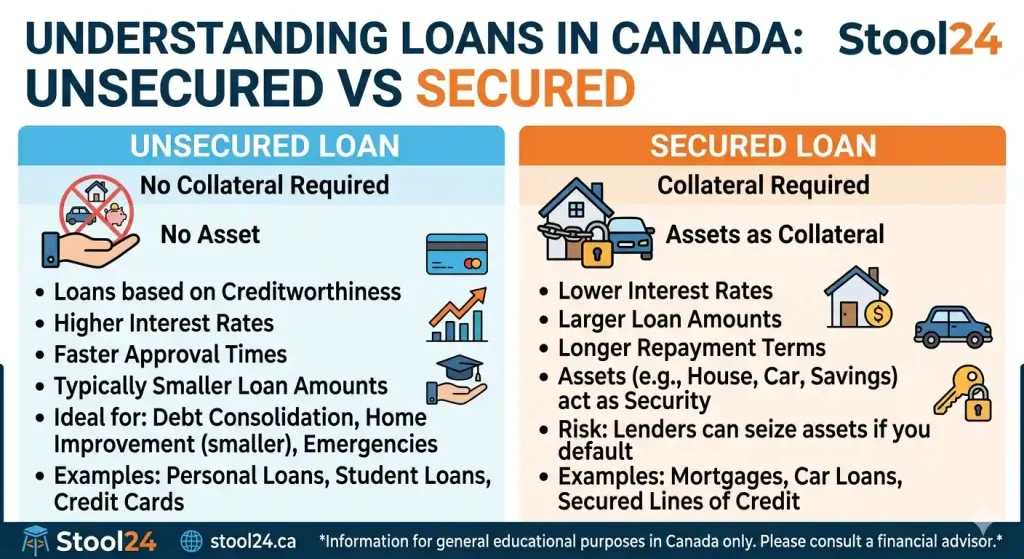

What Is a Secured and Unsecured Loan in Canada?

Before comparing them, it helps to understand how each loan type works. The core difference lies in collateral—an asset that backs the loan and reduces risk for the lender.

What Is a Secured Loan?

A secured loan is backed by collateral such as a home, vehicle, or savings account. If the borrower cannot repay the loan, the lender can legally seize the asset to recover the debt.

Common secured loans in Canada include:

- Mortgages

- Auto loans

- Home equity loans

- Secured lines of credit

Because lenders have protection through collateral, these loans typically offer lower interest rates and larger borrowing limits.

What Is an Unsecured Loan?

An unsecured loan does not require collateral. Approval depends mainly on your credit score, income stability, and debt-to-income ratio.

Examples of unsecured loans include:

- Personal loans

- Credit cards

- Student loans

- Some short-term consumer loans

Since lenders take on more risk, interest rates are usually higher than secured borrowing options.

Why Lenders Treat These Loans Differently

Lenders assess risk when approving any loan. With secured lending, collateral protects the lender if payments stop. Without that protection, unsecured loans rely heavily on credit history.

This difference explains why secured loans often have lower interest rates and easier approval for larger amounts.

In Canada, lenders also report payment behaviour to credit bureaus such as Equifax Canada and TransUnion Canada, which means both loan types can influence your credit score.

Unsecured vs Secured Loan Canada: Key Differences

Borrowers often compare these loan types before applying. The table below highlights the main differences Canadians should understand before choosing one.

This table compares key features of secured and unsecured loans.

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral | Required (home, car, savings) | Not required |

| Interest Rates | Lower | Higher |

| Loan Amount | Higher borrowing limits | Usually smaller amounts |

| Approval Requirements | Collateral plus credit check | Credit score and income only |

| Risk | Possible loss of asset | Credit score damage |

According to the Financial Consumer Agency of Canada, borrowing costs vary widely depending on credit score and loan type.

Secured loans may have interest rates under 10%, while unsecured personal loans can exceed 20% for borrowers with weaker credit.

Examples of Secured and Unsecured Loans in Canada

Looking at real loan products helps make the comparison easier. Most Canadians already use at least one secured or unsecured borrowing product.

Common Secured Loans

These loans are tied to valuable assets.

- Mortgage loans for buying property

- Auto loans for purchasing vehicles

- Home equity loans or HELOCs

- Secured credit cards

Because collateral reduces lender risk, these loans usually offer lower interest rates and longer repayment terms.

Common Unsecured Loans

Unsecured borrowing is much more flexible. The money can often be used for almost any purpose.

- Personal loans

- Credit card balances

- Emergency financing

- Short-term consumer loans

For example, someone dealing with an unexpected repair bill may choose an unsecured personal loan because approval is faster.

Real-World Borrowing Example

A homeowner planning a $25,000 renovation may use a home equity loan because interest rates are lower.

Meanwhile, a renter who needs $5,000 quickly might choose an unsecured personal loan because they have no property to offer as collateral.

Pros and Cons of Secured vs Unsecured Loans

Every borrowing option has advantages and risks. Understanding these trade-offs helps borrowers make smarter financial decisions.

Pros and Cons

Advantages of Secured Loans

- Lower interest rates

- Higher borrowing limits

- Easier approval with weaker credit

- Longer repayment periods

Disadvantages of Secured Loans

- Collateral is required

- Approval can take longer

- Risk of losing assets if payments stop

Advantages of Unsecured Loans

- No asset required

- Faster approval

- Flexible use of funds

Disadvantages of Unsecured Loans

- Higher interest rates

- Lower borrowing limits

- Stricter credit requirements

Understanding these differences helps borrowers avoid high-interest debt or unnecessary financial risk.

How Canadian Lenders Evaluate Loan Applications

Lenders in Canada look beyond the loan type. They analyze several factors before approving any borrower.

Credit Score Requirements

Your credit score is one of the most important factors. Scores above 680 generally qualify for better unsecured loan rates, while lower scores may require secured borrowing.

Both Equifax Canada and TransUnion Canada track payment history, credit utilization, and outstanding debt.

Debt-to-Income Ratio

Lenders compare your monthly debt payments to your income. A lower debt-to-income ratio improves approval chances.

Many Canadian lenders prefer borrowers with DTI below 40%.

Employment and Income Stability

Stable employment reassures lenders that you can handle monthly payments. Self-employed applicants may need to provide additional income verification.

Collateral Value for Secured Loans

When applying for a secured loan, lenders also evaluate the asset being used as collateral.

A home with strong equity or a newer vehicle increases approval chances and may lead to better rates.

When Should You Choose a Secured or Unsecured Loan?

Borrowers often ask which option is better. The answer depends on the size of the loan and the risk you’re willing to take.

Situations Where a Secured Loan Makes Sense

- Large purchases like homes or vehicles

- Debt consolidation with lower interest rates

- Borrowers with limited credit history

When an Unsecured Loan Is Better

- Emergency expenses

- Borrowers without assets

- Small or short-term borrowing needs

One practical approach is estimating your monthly payments before applying.

Use a quick estimate to see how interest rates affect your monthly payment.

[ Personal Loan Payment Calculator ]

You can also review current lending trends and borrowing costs using resources like Canadian personal loan interest rate guides to understand what lenders are offering today.

Many borrowers also compare tax-related financial tools within the tax toolkit to better plan borrowing decisions alongside income and deductions.

Risks to Consider Before Borrowing

Borrowing always carries risk, especially when large amounts or valuable assets are involved.

What Happens If You Default on a Secured Loan

If payments stop, the lender can seize the collateral. In mortgage cases, this could lead to foreclosure.

Vehicle loans may lead to repossession if borrowers fall significantly behind on payments.

What Happens If You Default on an Unsecured Loan

Unsecured loans cannot seize assets directly, but the consequences can still be serious.

Missed payments can lead to collection actions, legal claims, and long-term credit damage.

How Loans Affect Your Credit Score

Payment history accounts for roughly 35% of your credit score according to Canadian credit bureau scoring models.

Consistent on-time payments improve credit standing and may unlock better borrowing options later.

Common Mistakes Canadians Make When Choosing a Loan

Many borrowers rush into financing without understanding long-term costs. A few simple mistakes can make borrowing far more expensive.

- Ignoring the total interest cost of a loan

- Using high-interest unsecured loans for large purchases

- Risking important assets as collateral unnecessarily

- Failing to compare lenders and interest rates

Taking time to review rates, repayment terms, and borrowing limits can prevent serious financial stress later.

FAQS For Unsecured vs Secured Loan Canada

What is the main difference between secured and unsecured loans in Canada?

Secured loans require collateral, such as a home or vehicle, while unsecured loans do not. Collateral reduces lender risk, resulting in lower interest rates for secured loans, whereas unsecured loans rely on creditworthiness and typically carry higher rates.

Which loan type is easier to get approved for in Canada?

Secured loans are often easier to approve if you have collateral, even with a lower credit score. Unsecured loans require strong credit and stable income, making approval more challenging for borrowers with weaker credit history.

Do unsecured loans have higher interest rates than secured loans?

Yes, unsecured loans generally have higher interest rates because lenders face more risk without collateral. Secured loans offer lower rates due to the safety of an asset backing the loan.

Can I get an unsecured loan with bad credit in Canada?

It is possible but challenging. Some lenders specialize in personal loans for borrowers with lower credit scores, but interest rates will likely be higher, and borrowing limits may be smaller.

What happens if I default on a secured loan?

If you default on a secured loan, the lender can seize the collateral used to back the loan, such as your home or car. This makes repayment essential to avoid asset loss.

When should I choose a secured loan over an unsecured loan?

Choose a secured loan for large purchases, debt consolidation, or if you want lower interest rates. Unsecured loans are better for short-term borrowing or when you don’t have assets to use as collateral.

How do secured and unsecured loans affect my credit score in Canada?

Both types of loans impact your credit score. On-time payments improve your credit, while missed payments on either secured or unsecured loans can damage your credit report and make future borrowing more difficult.

Quick Summary

Understanding unsecured vs secured loan Canada helps borrowers make smarter financial choices.

- Secured loans require collateral but offer lower interest rates.

- Unsecured loans are faster to obtain but typically cost more.

- Lenders evaluate credit score, income stability, and debt ratios.

- Large purchases often favour secured loans.

- Short-term borrowing may work better with unsecured financing.

The right loan depends on your financial situation, risk tolerance, and borrowing goals. Taking time to compare options can save thousands in interest and help protect your financial stability.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is the main difference between secured and unsecured loans in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Secured loans require collateral, such as a home or vehicle, while unsecured loans do not. Collateral reduces lender risk, resulting in lower interest rates for secured loans, whereas unsecured loans rely on creditworthiness and typically carry higher rates.” } }, { “@type”: “Question”, “name”: “Which loan type is easier to get approved for in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Secured loans are often easier to approve if you have collateral, even with a lower credit score. Unsecured loans require strong credit and stable income, making approval more challenging for borrowers with weaker credit history.” } }, { “@type”: “Question”, “name”: “Do unsecured loans have higher interest rates than secured loans?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, unsecured loans generally have higher interest rates because lenders face more risk without collateral. Secured loans offer lower rates due to the safety of an asset backing the loan.” } }, { “@type”: “Question”, “name”: “Can I get an unsecured loan with bad credit in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “It is possible but challenging. Some lenders specialize in personal loans for borrowers with lower credit scores, but interest rates will likely be higher, and borrowing limits may be smaller.” } }, { “@type”: “Question”, “name”: “What happens if I default on a secured loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “If you default on a secured loan, the lender can seize the collateral used to back the loan, such as your home or car. This makes repayment essential to avoid asset loss.” } }, { “@type”: “Question”, “name”: “When should I choose a secured loan over an unsecured loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Choose a secured loan for large purchases, debt consolidation, or if you want lower interest rates. Unsecured loans are better for short-term borrowing or when you don’t have assets to use as collateral.” } }, { “@type”: “Question”, “name”: “How do secured and unsecured loans affect my credit score in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Both types of loans impact your credit score. On-time payments improve your credit, while missed payments on either secured or unsecured loans can damage your credit report and make future borrowing more difficult.” } } ] }