A property priced at $500,000 renting for $2,200 a month might look like a great deal—but is it actually profitable? That’s where knowing how to calculate rental yield becomes essential. Without it, you’re guessing instead of making a smart investment decision.

This guide breaks down how to calculate rental yield in Canada using simple formulas, real examples, and practical insights. You’ll also learn how to factor in expenses, compare returns, and avoid common mistakes that can quietly eat into your profits.

Table of Contents

How to Calculate Rental Yield in Canada (Complete Investor Guide)

What Is Rental Yield and Why It Matters

Rental yield measures how much income your property generates compared to its value. It’s one of the fastest ways to assess whether a real estate investment is worth considering.

Instead of relying on property appreciation alone, yield focuses on actual cash return. This matters even more in high-priced markets where buying costs are steep but rental income doesn’t always keep up.

Rental Yield Explained in Simple Terms

Rental yield is expressed as a percentage. It shows how much annual rental income you earn relative to the purchase price of the property.

Why Investors Use Rental Yield

Investors use rental yield to compare properties quickly. A higher yield usually means better income potential, though it often comes with trade-offs like location or property condition.

Rental Yield vs Property Appreciation

Yield focuses on income today, while appreciation looks at long-term price growth. Smart investors consider both when evaluating opportunities.

Rental Yield Formula Explained (Step-by-Step)

To calculate rental yield, you only need two numbers: annual rental income and property price. The formula is simple but powerful when used correctly.

Basic Formula to Calculate Rental Yield

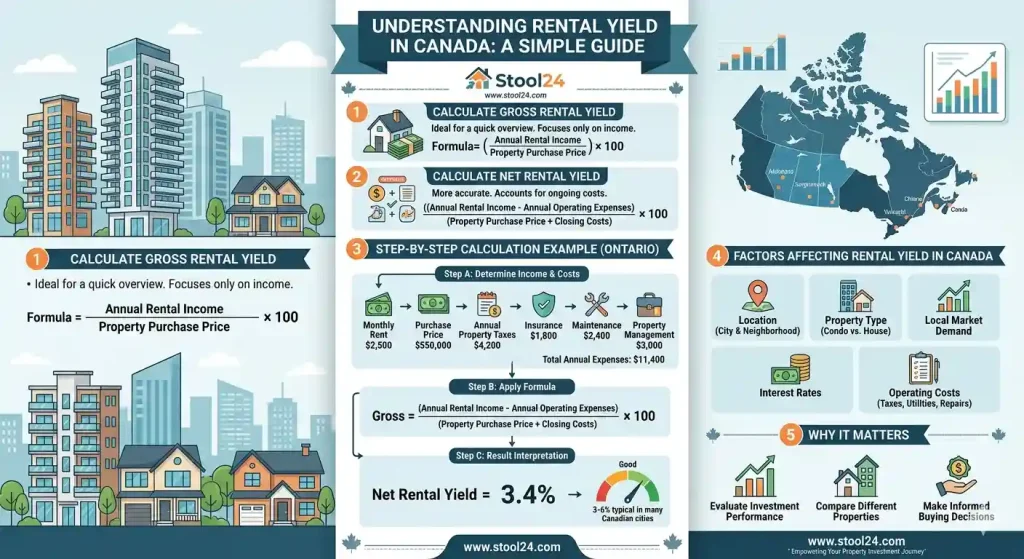

Rental Yield (%) = (Annual Rent ÷ Property Price) × 100

For example, if your property generates $24,000 per year and costs $400,000, your yield is 6%.

How to Calculate Rental Yield with Monthly Rent

If you only know monthly rent, multiply it by 12. Then plug that number into the formula.

Quick math, but often overlooked.

Even small calculation mistakes can lead to poor decisions. Always double-check your numbers before evaluating a deal, especially when comparing multiple properties.

Common Mistakes When Using the Formula

- Using estimated rent instead of actual market data

- Ignoring vacancy periods

- Forgetting closing costs in total investment

Gross vs Net Rental Yield (Key Differences)

Not all rental yield calculations are equal. Gross yield gives a quick overview, while net yield provides a more realistic picture.

What Is Gross Rental Yield

Gross yield uses total rental income without subtracting expenses. It’s fast but not always accurate for decision-making.

What Is Net Rental Yield

Net yield includes operating costs, giving a clearer view of actual returns. Most experienced investors rely on this metric.

Expenses Included in Net Rental Yield

- Property taxes

- Insurance

- Maintenance and repairs

- Vacancy allowance

- Property management fees

This table compares Gross vs Net Rental Yield:

| Factor | Gross Yield | Net Yield |

|---|---|---|

| Expenses Included | No | Yes |

| Accuracy | Basic estimate | Realistic return |

| Use Case | Quick comparison | Investment decisions |

How to Calculate Rental Yield in Canada (Real Examples)

Real-world examples make it easier to understand how rental yield works across different markets.

Example 1: Condo in Toronto

Purchase price: $650,000

Monthly rent: $2,500

Annual rent: $30,000

Gross yield = 4.6%

After expenses, net yield may drop to around 3.2%.

Example 2: Suburban Property

Purchase price: $450,000

Monthly rent: $2,200

Gross yield = 5.8%

Example 3: Small-Town Investment Property

Purchase price: $300,000

Monthly rent: $1,800

Gross yield = 7.2%

Smaller markets often deliver higher yields but may come with higher vacancy risks.

What Is a Good Rental Yield in Canada?

Rental yield varies widely depending on location and property type. In major cities like Toronto or Vancouver, yields are typically lower due to high property prices.

According to insights from Canada Mortgage and Housing Corporation, rental demand remains strong, but affordability challenges impact returns.

Average Rental Yields by City

- Toronto: 3%–5%

- Vancouver: 3%–4%

- Calgary: 5%–7%

- Smaller cities: 6%–9%

High-Yield vs Low-Yield Markets

High-yield areas often have lower property prices but may lack strong appreciation potential.

How Interest Rates Impact Rental Yield

Changes from the Bank of Canada directly affect mortgage costs, which can reduce net yield significantly.

Rental Yield vs ROI vs Cash Flow

Rental yield is just one piece of the puzzle. To fully understand profitability, you need to look at other metrics too.

Key Differences Explained

Yield measures income efficiency, ROI includes total return, and cash flow tracks monthly profit after expenses.

This table compares Yield vs ROI vs Cash Flow:

| Metric | Focus | Best Use |

|---|---|---|

| Rental Yield | Income vs price | Quick comparison |

| ROI | Total return | Long-term analysis |

| Cash Flow | Monthly profit | Income planning |

When Rental Yield Can Be Misleading

A property may have a high yield but still generate negative cash flow if mortgage payments are high.

Which Metric Investors Should Prioritize

Experienced investors combine all three metrics instead of relying on just one.

Advanced Factors That Affect Rental Yield

Several hidden factors can impact your final yield calculation.

Mortgage and Financing Structure

Higher interest rates reduce net yield. Fixed vs variable rates also play a role.

Vacancy Rate and Tenant Risk

Even a 5% vacancy rate can significantly lower your annual income.

Taxes and Hidden Costs

Using tools like the tax toolkit helps estimate your real after-tax return more accurately.

Property Type (Condo vs House vs Multi-unit)

Multi-unit properties often offer higher yields but require more management.

How to Improve Your Rental Yield (Expert Tips)

Improving rental yield doesn’t always mean raising rent. Strategic changes can make a big difference.

Increase Rental Income Strategically

- Add furnished options

- Include utilities

- Offer short-term rentals where legal

Reduce Operating Costs

Energy-efficient upgrades can lower long-term expenses.

Choose High-Yield Locations

Look beyond major cities. Smaller markets often provide better returns.

Value-Add Renovations

Simple upgrades like kitchen improvements can justify higher rent.

To explore long-term gains alongside yield, check this guide on property appreciation in Canada.

Want quick numbers without manual math? Try a calculator.

[ Calculate Your Rental Yield Now ]

Rental Property Calculator

Common Mistakes to Avoid When Calculating Rental Yield

Even small errors can lead to poor investment decisions.

Ignoring Hidden Costs

Unexpected repairs and vacancies can reduce returns quickly.

Overestimating Rental Income

Always base estimates on actual market data, not assumptions.

Confusing Yield with Profit

High yield doesn’t always mean strong cash flow or long-term gain.

FAQS For Calculate Rental Yield

How do you calculate rental yield in Canada?

To calculate rental yield, divide your annual rental income by the property price and multiply by 100. For example, $24,000 annual rent on a $400,000 property equals a 6% yield. For accuracy, always compare both gross and net yield using real expenses.

What is a good rental yield in Canada?

A good rental yield in Canada typically ranges between 4% and 8%, depending on location and property type. Major cities like Toronto often sit closer to 3%–5%, while smaller markets can reach higher yields. Always balance yield with growth potential and risk.

What expenses should be included in net rental yield?

Net rental yield should include property taxes, insurance, maintenance, vacancy costs, and management fees. These expenses reduce your actual return and give a more realistic performance measure. Ignoring them can make a property seem more profitable than it really is.

Is rental yield the same as ROI?

No, rental yield and ROI measure different aspects of a property investment. Rental yield focuses on annual income relative to property value, while ROI includes total return, including appreciation and costs. Both should be used together for better decision-making.

How does a mortgage affect rental yield?

A mortgage does not impact gross yield but significantly affects net yield and cash flow. Higher interest rates increase monthly payments, reducing your overall return. This is especially important in Canada, where rate changes can directly impact profitability.

Can rental yield predict property profitability?

Rental yield gives a quick snapshot of income potential but doesn’t guarantee profitability. It doesn’t account for financing, taxes, or long-term appreciation. Use it alongside cash flow and ROI for a complete financial picture.

What is the difference between gross and net rental yield?

Gross rental yield is calculated using total rental income before expenses, while net yield accounts for all costs. Net yield provides a more accurate reflection of real returns. Most experienced investors rely on net yield for decision-making.

Quick Summary

Rental yield helps you evaluate property income quickly, but it’s only part of the full investment picture. Always calculate both gross and net yield, factor in real expenses, and compare results across different markets.

Combine yield with ROI and cash flow analysis to make smarter decisions. With the right approach, you can avoid costly mistakes and identify properties that truly perform.