A Canadian investor logs into their brokerage account ready to add savings, but pauses for a moment. How much can they safely deposit this year without triggering penalties? Understanding the tfsa contribution limit canada rules solves that problem quickly. These limits control how much you can contribute to a Tax-Free Savings Account each year and how unused room accumulates over time.

This guide explains the current TFSA limits, the total lifetime room available to Canadians, and how withdrawals or missed contributions affect your available space. You’ll also learn how to calculate your own contribution room, avoid common mistakes, and use the account more strategically to grow tax-free investments.

Table of Contents

TFSA Contribution Limit Canada: Annual Limits, Lifetime Room, and Rules Explained

The tfsa contribution limit canada determines the maximum amount Canadians can deposit into their Tax-Free Savings Account each year. Introduced in 2009 by the federal government, the TFSA allows investment income and capital gains to grow completely tax-free.

Unlike many other registered accounts, unused contribution room does not disappear. According to guidance from the Canada Revenue Agency, unused room automatically carries forward indefinitely. That flexibility is a major reason why millions of Canadians rely on TFSAs for savings and long-term investing.

What Is a TFSA and Why Contribution Limits Matter

A TFSA is a registered savings account where investment earnings are not taxed. Canadians can hold various investments inside it, including stocks, ETFs, GICs, and mutual funds.

The contribution limit exists to balance tax advantages while maintaining fairness in the tax system. Without limits, high-income investors could shelter unlimited investment income.

How the Tax-Free Savings Account Works in Canada

When you deposit money into a TFSA, that amount counts toward your contribution room for the year. Once invested, any growth—whether from dividends, interest, or capital gains—remains tax-free even when withdrawn.

This makes the TFSA particularly useful for long-term investing.

Why the TFSA Contribution Limit Exists

The federal government sets an annual contribution limit to regulate how much tax-sheltered savings Canadians can accumulate each year. Limits are periodically adjusted to reflect economic changes and inflation.

Who Is Eligible to Contribute to a TFSA

Eligibility is simple. Canadians can contribute if they:

- Are at least 18 years old

- Have a valid Social Insurance Number

- Are a resident of Canada for tax purposes

Once eligible, contribution room begins accumulating every year—even if you never open a TFSA account.

That accumulated room can grow surprisingly large over time.

Someone who never contributed for several years might suddenly realize they can deposit tens of thousands of dollars without penalties, because unused limits keep adding up year after year.

TFSA Contribution Limit Canada (Current Annual Limit)

The annual TFSA limit determines how much new contribution room Canadians receive each year. For 2025, the maximum contribution limit remains $7,000.

This amount represents new room added to every eligible Canadian’s TFSA contribution space.

What Is the TFSA Contribution Limit for 2025?

The federal government sets the TFSA limit periodically. For several recent years, the annual increase has stayed between $6,000 and $7,000 depending on inflation adjustments.

Data from Statistics Canada shows that millions of Canadians contribute to their TFSA annually, with contributions often close to the yearly limit.

TFSA Contribution Limit Canada vs Total Contribution Room

The annual limit is only one piece of the puzzle. Your personal contribution room includes:

- Annual limits since you turned 18

- Unused room from previous years

- Withdrawals from earlier years

Because of these factors, your personal limit may be much higher than the current yearly cap.

How TFSA Limits Are Set by the Government

The Department of Finance reviews TFSA policies regularly. Adjustments typically appear in federal budget announcements and CRA updates.

These changes help keep the program aligned with inflation and long-term savings policy.

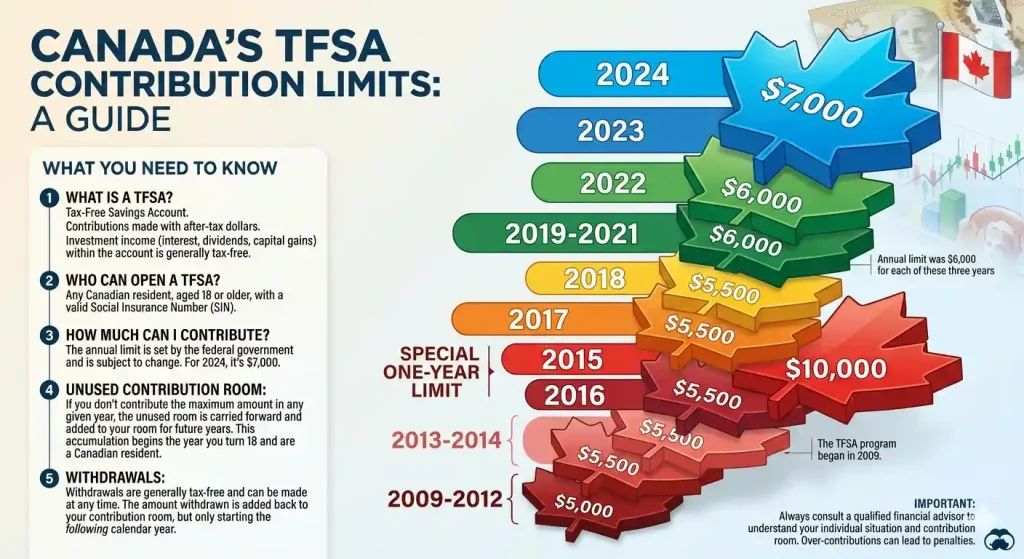

TFSA Contribution Limit History (2009–2025)

The table below shows how annual TFSA limits have changed since the account was introduced.

TFSA Contribution Limit History in Canada

| Year | Annual Limit |

|---|---|

| 2009–2012 | $5,000 |

| 2013–2014 | $5,500 |

| 2015 | $10,000 |

| 2016–2018 | $5,500 |

| 2019–2022 | $6,000 |

| 2023–2025 | $6,500–$7,000 |

Total Lifetime TFSA Contribution Room

If you were eligible since the program launched in 2009, your total TFSA contribution room now exceeds $95,000. That amount represents the combined limits for each year.

Example: Maximum TFSA Room if You Were 18 in 2009

Imagine someone who turned 18 in 2009 but never contributed to their TFSA until today. They could deposit nearly $95,000 at once without exceeding their contribution limit.

This is why reviewing unused TFSA space is an important step in financial planning.

How TFSA Contribution Room Works

Contribution room grows automatically every year and carries forward indefinitely. That rule makes the TFSA one of the most flexible savings accounts available in Canada.

Unused Contribution Room Carry Forward

If you contribute less than the annual limit, the remaining amount is added to your available room in future years. Nothing is lost.

How Withdrawals Affect TFSA Contribution Room

When you withdraw money from a TFSA, that amount gets added back to your contribution room in the following calendar year.

However, redepositing it during the same year could trigger an overcontribution.

How to Calculate Your TFSA Contribution Room

You can estimate your available room with a simple process.

- Add annual TFSA limits since you turned 18

- Subtract all contributions made so far

- Add withdrawals from previous years

Small calculations like this can help investors avoid costly penalties.

Curious how investment growth can expand your tax-free savings?

[Try the TFSA Growth Calculator]

Estimate your TFSA investment growth

TFSA Contribution Limit Canada: Example Scenarios

Real situations make TFSA rules easier to understand.

Example 1: New Investor

A 25-year-old who has never contributed could have tens of thousands of dollars available in contribution room. They could invest a large lump sum immediately.

Example 2: Withdrawal Scenario

If you withdraw $4,000 this year, that amount will be added back to your contribution room next year.

Example 3: Overcontribution Scenario

If your available room is $7,000 but you contribute $8,000, the extra $1,000 becomes an overcontribution.

Example 4: Late Starter Strategy

Someone who begins investing later in life can still catch up by using accumulated TFSA room.

TFSA Overcontribution Rules and CRA Penalties

Overcontributing to a TFSA triggers penalties administered by the CRA. These rules are strict and apply even if the mistake was unintentional.

What Happens If You Exceed the TFSA Limit

When contributions exceed your available room, the excess amount becomes subject to monthly penalties.

CRA Penalty Rate for Overcontributions

The CRA applies a tax of 1% per month on the highest excess amount in the account.

This penalty continues until the extra contribution is removed.

How to Fix a TFSA Overcontribution

If you discover an overcontribution, act quickly:

- Withdraw the excess amount immediately

- Track future deposits carefully

- Review your CRA contribution records

Quick action can prevent unnecessary tax charges.

Expert Tips to Maximize Your TFSA Contribution Room

Financial planners often recommend using the TFSA alongside other tax-efficient accounts.

Best Investments to Hold in a TFSA

Growth-focused assets tend to benefit the most from tax-free compounding.

- Stocks

- Exchange-traded funds

- Dividend-producing investments

TFSA vs RRSP Strategy

For higher-income earners, understanding how RRSP contributions reduce taxable income can help balance long-term tax planning.

Common TFSA Contribution Mistakes

A few common mistakes include:

- Re-depositing withdrawals too early

- Ignoring contribution tracking

- Assuming CRA records are always updated instantly

Helpful calculators and planning tools are often included in the Tax Toolkit, where Canadians can explore different savings strategies and compare financial planning resources.

FAQS For TFSA Contribution Limit Canada

What is the TFSA contribution limit in Canada for 2025?

The annual TFSA contribution limit for 2025 is $7,000. This amount represents the maximum new room available to eligible Canadian residents for the year. If you have unused contribution room from previous years, you may be able to contribute significantly more.

What is the total TFSA contribution room since 2009?

If you were 18 years old in 2009 and remained eligible every year, the total cumulative TFSA contribution room now exceeds $95,000. This amount reflects the combined annual limits introduced since the program launched. Your personal limit may differ depending on age and past contributions.

Does unused TFSA contribution room carry forward?

Yes, unused TFSA contribution room automatically carries forward every year. If you do not use your full limit, the remaining amount is added to your available room in future years. This rule allows Canadians to make larger contributions later if needed.

What happens if I exceed the TFSA contribution limit?

If you contribute more than your allowed TFSA room, the Canada Revenue Agency applies a penalty tax of 1% per month on the excess amount. The penalty continues until the extra funds are removed from the account. Withdrawing the overcontribution quickly helps minimize the tax.

How do I check my TFSA contribution room?

You can check your TFSA contribution room through your CRA My Account online portal or by reviewing your latest notice of assessment. Financial institutions may also provide contribution tracking tools. However, it is important to keep your own records because CRA data may not always reflect recent transactions.

Do TFSA withdrawals increase my contribution room?

Yes, withdrawals from a TFSA are added back to your contribution room in the following calendar year. For example, if you withdraw $5,000 this year, that amount becomes available again next year. Re-depositing the funds in the same year could trigger an overcontribution.

Does investment growth affect the TFSA contribution limit?

No, investment gains inside a TFSA do not affect your contribution limit. Whether your investments grow to $20,000 or $200,000, that growth remains tax-free and does not reduce your contribution room. Only deposits and withdrawals impact your available limit.

Quick Summary

The tfsa contribution limit canada determines how much Canadians can deposit into their Tax-Free Savings Account each year. For 2025, the annual limit remains $7,000, while unused contribution room continues to carry forward indefinitely.

Understanding how contribution room, withdrawals, and penalties work helps Canadians avoid mistakes and take full advantage of this powerful tax-free savings account.