A new entrepreneur sits down with a business idea, a rough budget, and one big question: where will the startup capital come from? For many founders, the answer starts with a startup loan Canada guide that explains how funding actually works in the Canadian financial system. Launching a company often requires equipment, inventory, marketing, and working capital before revenue begins.

This guide explains how startup loans work in Canada, what lenders look for, and which funding programs may help new businesses secure capital. You’ll also learn practical steps to improve approval chances, compare funding options, and avoid common mistakes that prevent entrepreneurs from getting the financing they need.

Table of Contents

Startup Loan Canada Guide How to Get Funding for a New Business

Starting a business requires more than a strong idea. In Canada, entrepreneurs often need capital for equipment, renovations, hiring, or operating expenses. A structured startup loan strategy helps new founders access funding without risking unnecessary debt.

This startup loan Canada guide breaks down the available options, eligibility requirements, and practical steps that help new businesses secure financing. Understanding how lenders evaluate startups is the first step toward building a successful funding strategy.

Understanding Startup Loans in Canada

Many new founders ask whether startups can even qualify for financing. The short answer is yes, but lenders usually evaluate both the business plan and the entrepreneur’s personal financial profile.

What Is a Startup Business Loan?

A startup loan provides capital to launch a new company before the business has established revenue. The funds can cover expenses such as equipment, leasehold improvements, inventory, or marketing campaigns.

In Canada, startup loans are often structured with personal guarantees or government-backed programs. This reduces risk for lenders while allowing entrepreneurs to access funding earlier in the business lifecycle.

How Startup Loans Work in Canada

Canadian lenders typically review several factors before approving startup financing. These include credit history, industry experience, financial projections, and the strength of the business plan.

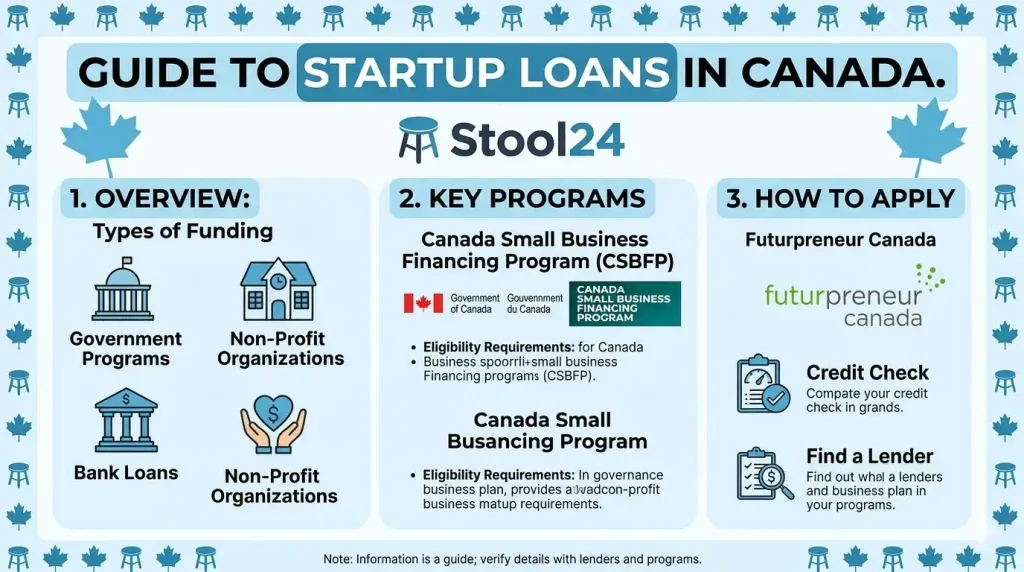

Programs supported by the federal government also play a role. According to Innovation, Science and Economic Development Canada, the Canada Small Business Financing Program helps small businesses access loans by sharing risk with lenders.

When a Startup Should Consider a Business Loan

Startup loans make the most sense when the borrowed capital directly contributes to growth. Businesses commonly use funding for:

- Purchasing equipment or vehicles

- Renovating retail or office space

- Buying initial inventory

- Funding early marketing campaigns

- Covering early operating expenses

Not every startup should borrow immediately. But when the investment clearly supports growth, financing can accelerate the launch phase.

And sometimes that early capital makes the difference between a slow start and a strong market entry.

Canada’s startup ecosystem continues to grow. According to Statistics Canada, small businesses represent more than 97% of employer businesses in the country. Many of them began with some form of startup financing.

Types of Startup Loans Available in Canada

New entrepreneurs have several funding options. Understanding the differences helps founders choose the right financing structure for their situation.

Government-Backed Startup Loans

Government programs reduce lender risk and improve startup access to financing. These programs often offer more favourable repayment terms than traditional loans.

Canada Small Business Financing Program

The Canada Small Business Financing Program allows lenders to provide loans backed by the federal government. Businesses can borrow funds for equipment, real estate improvements, and other startup costs.

You can learn more about how these programs compare to U.S. financing programs through this detailed guide on the Canadian SBA equivalent.

Provincial Funding Programs

Many provinces offer additional startup financing programs, particularly for technology, agriculture, and regional development businesses.

Organizations such as Business Development Bank of Canada also provide specialized funding and advisory support for early-stage companies.

Startup Loans From Banks and Credit Unions

Traditional lenders remain one of the most common funding sources. Major Canadian banks evaluate startup applications based on:

- Personal credit score

- Industry experience

- Business plan quality

- Available collateral

While banks may have stricter requirements, they often provide competitive interest rates once approved.

Alternative Startup Financing Options

Not every founder qualifies for a bank loan immediately. Alternative funding sources include:

- Microloans

- Online lenders

- Startup accelerators

- Angel investor networks

The table below compares common startup funding sources available in Canada.

| Funding Source | Typical Loan Amount | Requirements | Best For |

|---|---|---|---|

| Government Programs | $50,000 – $1,000,000 | Business plan and eligible expenses | Equipment and expansion |

| Bank Loans | $25,000 – $500,000 | Strong credit and collateral | Established entrepreneurs |

| Microloans | $5,000 – $50,000 | Basic credit and business plan | Small startups |

| Online Lenders | $10,000 – $250,000 | Flexible requirements | Fast funding |

Startup Loan Canada Guide: Eligibility and Requirements

Lenders ask similar questions when reviewing startup loan applications. Understanding these factors helps founders prepare before submitting an application.

Credit Score and Personal Financial History

Because new businesses have limited financial history, lenders often rely on the founder’s personal credit profile. A credit score above 680 generally improves approval chances.

Strong credit signals responsible borrowing behaviour, which reduces perceived risk for lenders.

Business Plan and Financial Projections

A well-structured business plan demonstrates that the entrepreneur understands the market and potential risks.

Lenders often expect projections covering:

- Startup costs

- Revenue forecasts

- Operating expenses

- Break-even timelines

Collateral and Personal Guarantees

Some startup loans require collateral such as equipment, property, or personal assets. Personal guarantees are also common for early-stage businesses.

These guarantees protect lenders in case the business cannot repay the loan.

Time in Business and Revenue Expectations

While startup loans target new companies, some lenders still require early revenue projections or industry experience. Demonstrating expertise in the chosen field can strengthen the application significantly.

Step-by-Step Guide to Getting a Startup Loan in Canada

Entrepreneurs often feel overwhelmed by the loan application process. Breaking the process into clear steps makes it easier to navigate.

Step 1 – Define Your Startup Funding Needs

Start by calculating total startup costs. Include equipment, inventory, licensing, marketing, and operating capital for at least the first six months.

Step 2 – Create a Strong Business Plan

Lenders want to see realistic projections and a clear growth strategy. A solid plan shows how the borrowed funds will generate revenue.

Step 3 – Compare Loan Programs and Lenders

Different lenders offer different advantages. Government programs often provide lower interest rates, while alternative lenders may approve applications faster.

Step 4 – Prepare Required Documents

Common documents include identification, financial statements, business registration documents, and financial projections.

Step 5 – Submit the Application and Negotiate Terms

Once approved, review loan terms carefully. Pay attention to interest rates, repayment schedules, and potential fees.

If you’re estimating payments for a business loan, a quick calculation helps clarify affordability.

Try estimating your monthly repayment with a Business Loan Calculator.

Example: How a Canadian Startup Secures Funding

Consider a simple example of a small retail startup opening in a mid-size Canadian city.

Example Scenario: Opening a Retail Business

The founder needs capital for store renovation, shelving, inventory, and marketing. The estimated startup cost totals $120,000.

Startup Budget Breakdown

The table below shows a simplified startup budget example.

| Startup Expense | Estimated Cost |

|---|---|

| Store Renovation | $40,000 |

| Inventory | $35,000 |

| Equipment | $20,000 |

| Marketing | $15,000 |

| Working Capital | $10,000 |

Loan Structure and Monthly Payments

The entrepreneur secures a $100,000 government-supported startup loan and contributes $20,000 in personal savings. Monthly payments remain manageable while allowing the business to grow.

Common Startup Loan Mistakes Entrepreneurs Make

Many startup loan applications fail because founders overlook basic preparation steps.

Applying Without a Clear Business Plan

Lenders want to understand how the business will generate revenue. A vague plan often leads to immediate rejection.

Borrowing Too Much or Too Little

Borrowing too little can stall growth, while borrowing too much increases financial risk. Accurate budgeting is critical.

Ignoring Loan Terms and Interest Costs

Some entrepreneurs focus only on loan approval and overlook the long-term cost of financing. Interest rates and repayment terms significantly impact business cash flow.

Not Exploring Government Funding Programs

Many founders skip government funding options entirely, even though these programs often offer better conditions than private lenders.

Expert Tips to Increase Startup Loan Approval Chances

Experienced lenders often see the same patterns among successful applicants.

Improve Your Personal Credit Score

Paying down existing debts and correcting credit report errors can raise approval chances quickly.

Build a Strong Financial Projection

Lenders trust numbers backed by realistic assumptions. Demonstrating market demand strengthens credibility.

Use Government Programs to Reduce Risk

Programs backed by federal agencies reduce lender exposure, which often increases approval chances.

Start With Smaller Funding Options

Some entrepreneurs secure smaller loans first to establish a repayment track record before applying for larger funding.

Entrepreneurs also rely on financial planning resources such as the tax toolkit to better understand deductions, business taxes, and financial planning strategies that affect long-term profitability.

FAQS For startup loan canada guide

Can you get a startup loan in Canada with no revenue?

Yes, some lenders offer startup loans even if the business has not generated revenue yet. Approval usually depends on the founder’s credit score, business plan, and industry experience. Government-backed programs and microloans can also help early-stage entrepreneurs access funding before sales begin.

What government programs help startups get loans in Canada?

One of the most widely used options is the Canada Small Business Financing Program, which helps businesses access loans through participating lenders. Organizations like the Business Development Bank of Canada and Futurpreneur Canada also provide financing and mentorship for early-stage companies.

How much can you borrow for a startup business in Canada?

The amount depends on the lender, business type, and loan program. Government-backed programs may allow funding up to $1 million for certain business assets and improvements. Smaller startups often begin with loans ranging from $10,000 to $250,000 depending on their needs and credit profile.

What credit score is needed for a startup business loan in Canada?

Most traditional lenders prefer a personal credit score of around 680 or higher. A stronger credit history improves approval chances and may help secure better interest rates. Some alternative lenders and microloan programs may accept lower scores if the business plan is strong.

Are startup business loans difficult to get in Canada?

Startup loans can be challenging because new businesses usually lack financial history. However, lenders may approve funding if the entrepreneur has good credit, a detailed business plan, and realistic financial projections. Government-supported programs can also improve approval chances.

What documents are required when applying for a startup loan in Canada?

Most lenders request a business plan, financial projections, identification, and personal credit information. Some may also require proof of business registration, cost estimates, and collateral details. Preparing these documents in advance can significantly speed up the approval process.

Are there grants available instead of startup loans in Canada?

Yes, certain government and regional programs offer grants that do not require repayment. These grants are often targeted at specific industries, innovation projects, or regional economic development. Entrepreneurs usually combine grants with loans to build a complete startup funding strategy.

Quick Summary

Launching a business requires planning, capital, and realistic financial expectations. A strong startup loan strategy helps entrepreneurs access the funding needed to turn ideas into operating businesses.

- Startup loans in Canada come from banks, government programs, and alternative lenders.

- Credit history and business plans play major roles in approval decisions.

- Government-supported programs often reduce risk for lenders.

- Careful budgeting and realistic projections increase approval chances.

- Using financial tools and planning resources helps entrepreneurs manage loan costs effectively.

For many founders, the right financing strategy becomes the foundation that allows a new business to launch, grow, and eventually thrive.