Choosing the right savings account can have a significant impact on your finances in Canada. Many Canadians struggle to decide between an RRSP and a TFSA, especially when planning for both short-term goals and long-term retirement. Understanding the rrsp vs tfsa difference is key to making the best choice for your tax situation and retirement strategy. In this guide, you will learn the main differences, contribution limits, tax implications, and practical scenarios to help you decide which account—or combination—fits your financial goals.

Table of Contents

RRSP vs TFSA Difference: Which Savings Account Is Better for Canadians?

Both RRSPs and TFSAs offer unique benefits, but they serve different purposes in your financial plan. While RRSP contributions are tax-deductible, TFSA withdrawals are tax-free. Knowing how each account works can help you maximize savings, reduce taxes, and plan for retirement efficiently.

Understanding the RRSP vs TFSA Difference

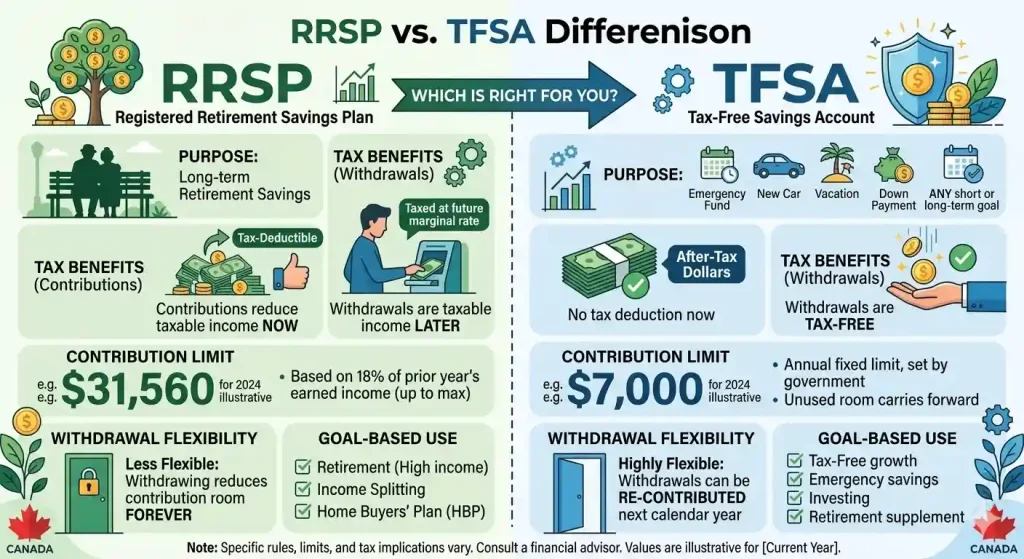

What Is an RRSP?

A Registered Retirement Savings Plan (RRSP) allows Canadians to contribute a portion of their income into a tax-advantaged account. Contributions reduce your taxable income for the year, potentially generating a tax refund. The investments inside grow tax-deferred until you withdraw the funds, usually during retirement when your income may be lower.

What Is a TFSA?

A Tax-Free Savings Account (TFSA) is a flexible account where contributions are made with after-tax dollars, meaning there is no immediate tax deduction. However, all investment growth and withdrawals are completely tax-free. This makes TFSAs ideal for both short-term savings and long-term growth without affecting government benefits.

Why Canadians Compare RRSP and TFSA

Understanding the rrsp vs tfsa difference helps determine which account maximizes tax efficiency and retirement planning. While RRSPs benefit high-income earners seeking immediate tax deductions, TFSAs offer greater flexibility and tax-free withdrawals for individuals in any income bracket.

RRSP vs TFSA Difference in Taxes and Withdrawals

How RRSP Contributions Reduce Taxable Income

RRSP contributions are deducted from your annual income, reducing the amount of tax owed. For instance, contributing $10,000 to an RRSP can lower taxable income from $75,000 to $65,000, possibly pushing part of your income into a lower tax bracket. This is particularly advantageous for Canadians in higher income brackets.

How TFSA Provides Tax-Free Withdrawals

Unlike RRSPs, withdrawals from a TFSA are not taxed. This means you can access your money at any time without impacting your tax liability or government benefits like OAS or GIS. The combination of tax-free growth and flexible access makes TFSAs ideal for emergency funds or large purchases.

Withdrawal Rules and Tax Impact

RRSP withdrawals are taxed as income in the year they are taken. Exceptions include the Home Buyers’ Plan (HBP) and Lifelong Learning Plan (LLP), which allow temporary tax-free withdrawals. TFSA withdrawals, however, are completely tax-free and the withdrawn amount can be recontributed the following year.

Estimate your tax impact using a quick calculator.

Calculate Your RRSP & TFSA Savings

Contribution Limits and Rules in Canada

RRSP Contribution Limits Explained

The CRA sets RRSP contributions at 18% of the previous year’s earned income, up to an annual maximum. Unused contribution room carries forward indefinitely, allowing Canadians to contribute more in future years. Over-contributions are subject to penalties.

TFSA Annual Contribution Limits

TFSA contribution limits are set annually by the government and also carry forward if unused. For 2026, the limit is $6,500, but unused room accumulates, allowing flexibility in contributions over time.

Carry-Forward Contribution Room

Both RRSP and TFSA accounts allow unused contribution room to be carried forward. This means Canadians can strategically plan contributions based on income fluctuations and financial goals.

What Happens if You Over-Contribute

Exceeding the allowed limits results in penalties. The CRA charges 1% per month on excess contributions beyond the tolerance threshold. Monitoring your contribution room helps avoid unnecessary fees.

RRSP vs TFSA Difference for Retirement Planning

RRSP Strategy for Retirement Income

RRSPs are ideal for Canadians expecting higher income now and lower income in retirement. Contributions reduce taxes today, and withdrawals in retirement are taxed at potentially lower rates. Converting RRSPs to RRIFs ensures a structured income stream in retirement.

TFSA Flexibility for Future Withdrawals

TFSAs provide unmatched flexibility for accessing funds anytime without tax implications. This is beneficial for supplementing retirement income or handling unexpected expenses.

Impact on Government Benefits (OAS / GIS)

RRSP withdrawals may affect income-tested benefits such as OAS and GIS, while TFSA withdrawals do not. Strategic planning between both accounts can protect benefits and optimize net income during retirement.

Real-Life Examples: When RRSP or TFSA Works Better

Scenario 1: Young Professional

A 25-year-old starting their career may prioritize a TFSA for flexibility and low taxable income, taking advantage of tax-free growth without needing deductions immediately.

Scenario 2: High-Income Earner

Someone earning $120,000 annually may benefit from maximizing RRSP contributions to reduce taxable income, then supplement with TFSA contributions for flexible savings.

Scenario 3: Approaching Retirement

For individuals nearing retirement, balancing RRSP withdrawals with TFSA funds can optimize taxes and income stability while preserving government benefits.

Explore detailed strategies using the RRSP Tax Deduction Benefits guide.

Common Mistakes Canadians Make With RRSP and TFSA

Ignoring Contribution Limits

Overlooking limits can trigger penalties. Always verify your available contribution room with CRA records.

Choosing RRSP Too Early in Career

Young Canadians in lower tax brackets may not benefit from RRSP deductions immediately. TFSA contributions can be more effective initially.

Withdrawing RRSP Funds Too Soon

Early withdrawals incur taxes and reduce long-term retirement growth. Use exceptions like HBP and LLP judiciously.

Not Using Both Accounts Together

Many Canadians miss the chance to combine RRSP and TFSA strategies. Leveraging both accounts maximizes tax savings and financial flexibility.

Expert Tips for Choosing Between RRSP and TFSA

Consider Your Current Tax Bracket

High-income earners can benefit more from RRSP deductions, while low-income earners may gain more flexibility from a TFSA.

Think About Future Income

Estimate income changes to decide when to use RRSPs or TFSAs. Planning ahead prevents tax surprises and maximizes benefits.

Combine Both Accounts for Maximum Flexibility

Many Canadians use a combination strategy: RRSPs for immediate tax savings, TFSAs for accessible growth. This approach balances retirement planning and liquidity.

Use Tax Planning Tools and Calculators

Calculators simplify decision-making by showing projected savings and tax benefits.

Leverage the tax toolkit to compare scenarios and plan contributions efficiently.

FAQS For RRSP vs TFSA Difference

What is the main difference between an RRSP and a TFSA?

RRSP contributions are tax-deductible and reduce your taxable income, while TFSA contributions are made with after-tax dollars and withdrawals are tax-free. RRSPs are best for retirement savings, whereas TFSAs offer flexible access to your funds.

Which is better to contribute to first: RRSP or TFSA?

It depends on your income and financial goals. High-income Canadians often prioritize RRSPs for immediate tax savings, while low-income or younger earners may benefit more from a TFSA’s flexibility and tax-free growth.

Do TFSA withdrawals affect government benefits?

No, TFSA withdrawals do not impact income-tested government benefits like OAS or GIS. RRSP withdrawals, however, are counted as taxable income and may affect these programs.

Can I have both an RRSP and a TFSA?

Yes, Canadians can contribute to both accounts simultaneously. Many use RRSPs for long-term retirement tax planning and TFSAs for short-term savings or emergency funds.

What happens if I exceed my contribution limit?

Exceeding RRSP or TFSA contribution limits results in penalties from the CRA. A 1% per month tax is applied on the excess contributions, so monitoring your contribution room is crucial.

How do RRSP and TFSA impact retirement planning?

RRSPs provide a structured income stream in retirement, and withdrawals are taxed. TFSAs offer additional tax-free income and flexibility, helping balance taxes and protect government benefits.

Can unused contribution room be carried forward?

Yes, both RRSP and TFSA accounts allow unused contribution room to be carried forward indefinitely. This enables Canadians to contribute more in future years based on income and savings goals.

Quick Summary

Understanding the rrsp vs tfsa difference is crucial for Canadian financial planning. RRSPs provide tax deductions and structured retirement income, while TFSAs offer flexibility and tax-free growth. Using both accounts strategically maximizes tax savings, retirement security, and financial flexibility throughout life.