Imagine weighing the choice between renting a condo in Toronto or buying a home in Calgary. The long-term financial outcome isn’t always obvious. While buying builds equity, it comes with upfront costs, maintenance, and potential market risks. Renting offers flexibility but no asset growth. In this article, we’ll explore a detailed renting vs buying long term comparison in Canada, breaking down costs, hidden fees, lifestyle factors, and practical scenarios to help you make an informed decision.

Table of Contents

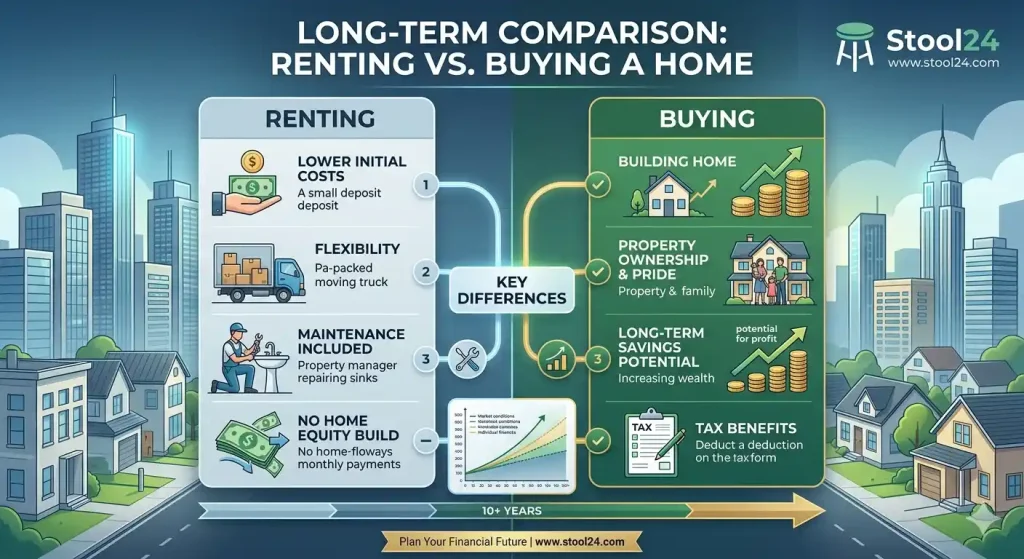

Renting vs Buying Long Term Comparison Which Is Better in Canada?

Understanding Renting vs Buying in the Long Term

Renting means paying a landlord monthly, while buying involves a mortgage and ownership responsibilities. For long-term Canadians, the decision is more than monthly payments—it impacts wealth, flexibility, and lifestyle choices over 10–25 years. Knowing these factors helps clarify whether renting or buying aligns with your financial goals.

Renting vs Buying Long Term Comparison Basics

Monthly costs differ significantly. Rent payments are predictable, but homeowners face mortgage fluctuations, property taxes, and maintenance. Flexibility is higher when renting, yet buying allows equity accumulation and potential appreciation.

True Cost Breakdown: Renting vs Buying in Canada

Let’s examine how upfront and ongoing costs shape the financial reality of both options.

Monthly and Upfront Costs Compared

Renting requires only a deposit and monthly rent. Buying demands a down payment, closing costs, and ongoing mortgage payments. For instance, a $500,000 home with a 20% down payment in Toronto could mean $100,000 upfront plus $3,000–$5,000 in closing fees. Monthly mortgage payments may range between $2,000–$2,500, depending on interest rates.

Hidden Costs of Homeownership

Maintenance, property taxes, and insurance add thousands annually. Unexpected repairs like a new roof or furnace can cost $10,000–$20,000. To learn more about these expenses, check the hidden costs of home guide.

Long-Term Cost of Renting

Rent tends to increase over time, often exceeding inflation. While renters avoid repair bills, they don’t build equity. Over 15–20 years, the total rent paid could match or surpass what a homeowner spends, especially in cities with rapidly rising housing prices.

Renting vs Buying Long Term Comparison: Financial Outcomes

This section analyzes net worth and opportunity costs over time to give a clear financial picture.

Net Worth After 5, 10, and 25 Years

Buying builds home equity while renters can invest savings elsewhere. For example, a 25-year-old in Vancouver investing $2,500 monthly instead of buying may accumulate $750,000 at a 6% annual return, while a homeowner builds equity and avoids rent but pays mortgage interest and taxes.

Opportunity Cost of Buying a Home

Investing a down payment in the stock market can yield higher returns than property appreciation in some markets. However, real estate can hedge against inflation and provide a tangible asset. Using a calculator, you can estimate your personalized rent vs buy scenario and projected net worth over time. Check your numbers here

Break-Even Point: When Buying Becomes Worth It

The break-even point depends on home price growth, mortgage rates, and rent increases. In Canada, studies show that staying in a home for 7–10 years typically offsets upfront buying costs, making ownership financially advantageous in the long term.

Canadian Market Factors That Change the Decision

Local conditions can significantly alter the renting vs buying calculation.

Interest Rates and Mortgage Trends

Higher mortgage rates increase monthly payments and slow equity growth. The Bank of Canada’s historical rates show fluctuations that can affect the optimal time to buy.

Housing Prices Across Canadian Cities

Toronto and Vancouver have seen double-digit annual appreciation, while smaller cities like Winnipeg or Halifax are slower but more affordable. Location impacts both potential equity growth and monthly affordability.

Inflation and Rent Growth in Canada

Rent tends to rise with inflation, affecting long-term renters more than owners with fixed-rate mortgages. According to CMHC data, Canadian rents have grown 3–5% annually in major urban centres over the past decade.

Lifestyle and Risk Factors Most People Ignore

Financial analysis isn’t the only factor—lifestyle choices matter too.

Flexibility vs Stability Trade-Off

Renting offers mobility for job changes or family needs. Buying provides a stable home base but reduces flexibility, especially if the market slows or home prices fall.

Market Risk and Housing Volatility

Housing markets fluctuate. Long-term ownership is generally safer, but unexpected downturns can delay equity accumulation. Risk-aware planning is essential for financial security.

Renting vs Buying in Uncertain Economies

High-interest periods make renting more attractive short-term, while stable low rates favor buying. Scenario planning helps balance risk and reward over decades.

Real-Life Scenarios: Which Option Wins?

Practical examples clarify abstract numbers.

Scenario 1: Young Professional (5-Year Horizon)

Renting might be better for career mobility and short-term savings, allowing investment in stocks or RRSPs. Buying may lock in costs but offers limited equity gain in such a short period.

Scenario 2: Family Planning Long-Term Stay (15+ Years)

Owning is generally advantageous. Home equity growth, tax benefits, and stability outweigh upfront costs. Using the tax toolkit can help maximize deductions and incentives for first-time buyers.

Scenario 3: Investor Mindset (Rent + Invest Strategy)

Renting while investing savings in a diversified portfolio can outperform buying if property appreciation is modest. Combining rent flexibility with smart investment decisions allows wealth accumulation without homeownership risks.

Common Mistakes in Renting vs Buying Decisions

- Ignoring hidden costs like repairs and taxes

- Overestimating home appreciation rates

- Not calculating the break-even point accurately

- Making decisions based purely on emotion

- Failing to account for lifestyle changes or mobility needs

Expert Tips to Decide: Rent or Buy in Canada

Follow these steps to make a confident decision:

- Define your timeline and life goals

- Calculate total costs including hidden fees

- Compare potential investment returns

- Assess flexibility and lifestyle needs

- Stress-test scenarios in uncertain markets

Quick Summary

Deciding between renting and buying in Canada requires a nuanced long-term perspective. Rent offers flexibility, while buying builds equity and can provide financial security over 10–25 years. Factoring in local market trends, lifestyle needs, hidden costs, and investment alternatives ensures a well-rounded choice. Use calculators and tools like the rent vs buy calculator to personalize your analysis and make an informed decision.

FAQS For Renting vs Buying Long Term Comparison

Is renting cheaper than buying in Canada long term?

Renting can be cheaper in the short term due to lower upfront costs and flexibility, but over 10–25 years, buying often builds more wealth through home equity. Your city, interest rates, and property growth play key roles in determining the cost-effectiveness.

How many years does it take for buying a home to be worth it?

In most Canadian cities, the break-even point is usually 7–10 years, depending on mortgage rates, property appreciation, and rent increases. Staying longer typically makes ownership financially advantageous compared to renting.

Should I rent or buy if I plan to move in a few years?

If you expect to move within 5 years, renting is generally more practical and cost-effective. Buying involves significant upfront costs and market risks that may not be recouped in a short period.

What are the hidden costs of buying a home in Canada?

Homeownership comes with maintenance, property taxes, insurance, and potential repairs. Learn more about these expenses through the hidden costs of home guide to budget effectively.

Can investing while renting outperform buying?

Yes, renting and investing savings in diversified assets can sometimes yield higher long-term returns, especially if property growth is moderate. This strategy balances mobility and financial growth.

How do Canadian market factors affect the rent vs buy decision?

Interest rates, housing prices, and rent growth differ by province and city. High rates or volatile markets may make renting attractive short-term, while stable conditions favor buying for long-term equity growth.

Are there tax incentives for first-time homebuyers in Canada?

Yes, programs like the First-Time Home Buyer Incentive, RRSP Home Buyers’ Plan, and local deductions can reduce upfront costs. Using a tax toolkit helps maximize these benefits.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “Is renting cheaper than buying in Canada long term?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Renting can be cheaper in the short term due to lower upfront costs and flexibility, but over 10–25 years, buying often builds more wealth through home equity. Your city, interest rates, and property growth play key roles in determining the cost-effectiveness.” } }, { “@type”: “Question”, “name”: “How many years does it take for buying a home to be worth it?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “In most Canadian cities, the break-even point is usually 7–10 years, depending on mortgage rates, property appreciation, and rent increases. Staying longer typically makes ownership financially advantageous compared to renting.” } }, { “@type”: “Question”, “name”: “Should I rent or buy if I plan to move in a few years?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “If you expect to move within 5 years, renting is generally more practical and cost-effective. Buying involves significant upfront costs and market risks that may not be recouped in a short period.” } }, { “@type”: “Question”, “name”: “What are the hidden costs of buying a home in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Homeownership comes with maintenance, property taxes, insurance, and potential repairs. Learn more about these expenses through the hidden costs of home guide to budget effectively.” } }, { “@type”: “Question”, “name”: “Can investing while renting outperform buying?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, renting and investing savings in diversified assets can sometimes yield higher long-term returns, especially if property growth is moderate. This strategy balances mobility and financial growth.” } }, { “@type”: “Question”, “name”: “How do Canadian market factors affect the rent vs buy decision?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Interest rates, housing prices, and rent growth differ by province and city. High rates or volatile markets may make renting attractive short-term, while stable conditions favor buying for long-term equity growth.” } }, { “@type”: “Question”, “name”: “Are there tax incentives for first-time homebuyers in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, programs like the First-Time Home Buyer Incentive, RRSP Home Buyers’ Plan, and local deductions can reduce upfront costs. Using a tax toolkit helps maximize these benefits.” } } ] }