A small change in mortgage rates can shift your monthly payment by hundreds of dollars. Right now, current mortgage interest rates Canada are fluctuating due to inflation, bond yields, and policy decisions from key institutions. If you’re planning to buy, refinance, or renew, understanding where rates stand today—and where they might go next—can save you thousands.

This guide breaks down current rates, explains what drives them, and helps you choose the best option based on your situation. You’ll also see real examples and practical strategies to lock in a better rate.

Table of Contents

Current Mortgage Interest Rates Canada (2026 Guide + Forecast)

Current Mortgage Interest Rates in Canada Today

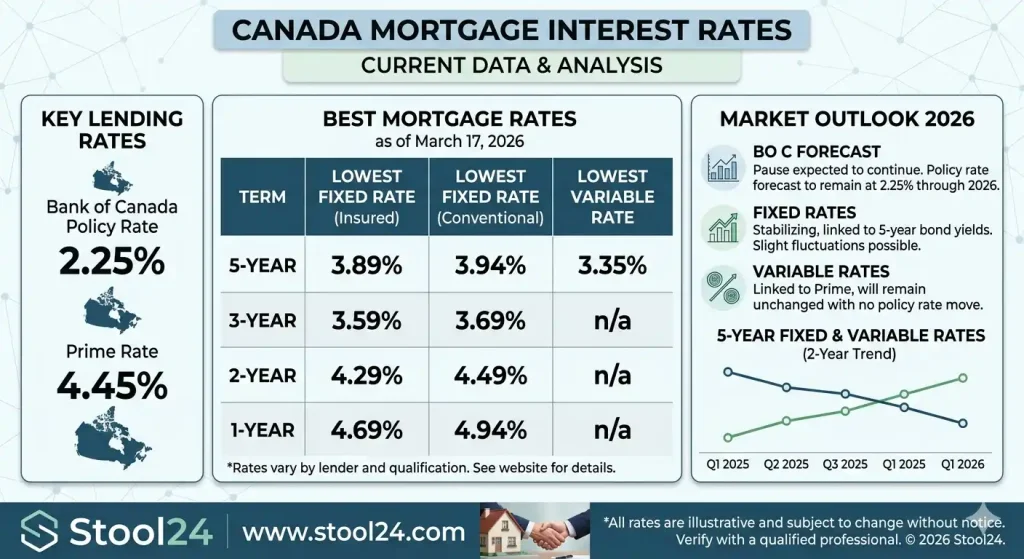

As of now, mortgage rates in Canada vary depending on term length, lender type, and borrower profile. Fixed rates are generally tied to bond yields, while variable rates move with the prime rate influenced by the Bank of Canada.

Most lenders offer competitive pricing, but advertised rates are not always what you’ll qualify for. Your credit score, down payment, and income stability all play a role.

Current Mortgage Interest Rates Canada by Term

This table shows typical ranges across major lenders.

| Mortgage Rate Comparison by Term (Canada) | Rate Range |

|---|---|

| 1-Year Fixed | 5.80% – 6.40% |

| 3-Year Fixed | 5.10% – 5.90% |

| 5-Year Fixed | 4.70% – 5.60% |

| 5-Year Variable | 5.90% – 6.50% |

Fixed vs Variable Mortgage Rates (Current Snapshot)

Choosing between fixed and variable comes down to risk tolerance and market outlook.

- Fixed rates: Stable payments, protection against increases

- Variable rates: Lower starting rate, but fluctuates

Best Mortgage Rates in Canada Right Now

Major banks like RBC and TD often advertise higher rates compared to brokers. Mortgage brokers can access wholesale rates and negotiate better deals for qualified borrowers.

How Mortgage Interest Rates Work in Canada

Mortgage rates are not random—they follow a system influenced by economic signals and lender strategies.

What Determines Mortgage Rates in Canada?

The Bank of Canada sets the overnight rate, which directly affects the prime rate used for variable mortgages. Inflation and employment data also influence future rate decisions.

Fixed vs Variable Rates Explained Clearly

Fixed rates are tied to government bond yields, especially the 5-year bond. Variable rates depend on the lender’s prime rate.

Pros and Cons:

- Fixed: Predictable, safer in rising markets

- Variable: Flexible, can save money if rates drop

Prime Rate vs Bond Yield (Key Drivers)

Variable mortgages move with prime rate changes, while fixed rates follow bond yields. According to the Bank of Canada, rate decisions are based heavily on inflation targets.

That’s why even if the Bank pauses rates, fixed mortgages can still rise or fall.

What Affects Current Mortgage Interest Rates Canada

Several factors shape the rates you see today.

Bank of Canada Rate Decisions

When the central bank raises rates, borrowing becomes more expensive. In 2023–2025, aggressive hikes pushed mortgage rates above 5%.

Canadian Bond Market Impact

Fixed mortgage rates closely follow 5-year government bond yields. A rise in bond yields usually leads to higher fixed rates.

Lender Risk & Borrower Profile

Lenders assess your financial risk before offering a rate. A higher credit score and larger down payment typically result in better pricing.

Insured vs Uninsured Mortgage Rates

Insured mortgages backed by Canada Mortgage and Housing Corporation often have lower rates because they carry less risk for lenders.

Mortgage Rate Comparison in Canada (Best Options)

Not all lenders offer the same value. Comparing options can reveal big savings.

Big Banks vs Mortgage Brokers vs Online Lenders

Banks provide convenience, but brokers often secure lower rates. Online lenders are gaining popularity for competitive pricing.

Fixed vs Variable: Which Is Better in 2026?

If rates are expected to fall, variable may offer savings. If uncertainty remains high, fixed provides stability.

Short-Term vs Long-Term Mortgage Rates

Short-term mortgages offer flexibility but require frequent renewals. Long-term options lock in rates but reduce flexibility.

This table compares key differences between mortgage types.

| Fixed vs Variable Mortgage Comparison | Fixed | Variable |

|---|---|---|

| Rate Stability | High | Low |

| Risk Level | Low | Medium-High |

| Potential Savings | Moderate | Higher (if rates drop) |

Example: How Much Your Mortgage Rate Affects Monthly Payments

Even a 1% difference in rate can significantly impact your monthly cost.

Scenario 1: 5-Year Fixed Rate Example

A $500,000 mortgage at 5% over 25 years results in roughly $2,900/month.

Scenario 2: Variable Rate Example

At 6%, the same mortgage jumps to around $3,200/month.

Small rate changes = big cost differences.

Want to calculate your exact payment?

Use a calculator to estimate your affordability based on income and expenses.

[ Calculate Your Mortgage Now ]

Mortgage Affordability Calculator Canada

You can also explore detailed payment breakdowns using tools like the Canadian mortgage calculator or understand your eligibility with the gross debt service ratio guide.

Mortgage Rate Forecast Canada (2026–2027)

Forecasting rates isn’t exact, but trends provide clues.

Expert Predictions & Trends

Many analysts expect gradual rate stabilization as inflation slows. According to CMHC, housing demand remains strong despite higher borrowing costs.

Will Mortgage Rates Go Down in Canada?

Rates may decline slightly, but a sharp drop is unlikely unless economic conditions weaken significantly.

What Buyers Should Do Right Now

Locking a rate early or choosing shorter terms can provide flexibility in uncertain markets.

How to Get the Lowest Mortgage Interest Rate in Canada

Getting the best rate requires strategy, not luck.

Step-by-Step Strategy to Secure the Best Rate

- Improve your credit score

- Increase your down payment

- Compare multiple lenders

- Lock your rate at the right time

Common Mistakes to Avoid

- Focusing only on interest rate instead of APR

- Not negotiating with lenders

- Ignoring prepayment penalties

Expert Tips Most Websites Miss

Use a mortgage broker to access hidden rates. Also, consider rate holds during volatile periods.

For broader financial planning tools, you can explore the tax toolkit to manage your overall finances more effectively.

Quick Summary

Mortgage rates in Canada are influenced by economic conditions, bond yields, and central bank policies. Fixed rates offer stability, while variable rates provide flexibility. Comparing lenders and understanding rate drivers can help you secure a better deal. Use calculators, plan ahead, and stay informed to make smarter mortgage decisions.

FAQS For Current Mortgage Interest Rates Canada

What are the current mortgage interest rates in Canada right now?

Current mortgage rates in Canada typically range between 4.7% and 6.5%, depending on the term and lender. Fixed rates are generally lower than variable rates at the moment due to bond market trends. Your exact rate will depend on your credit score, down payment, and income.

Will mortgage rates go down in Canada in 2026?

Mortgage rates may gradually decline if inflation continues to slow and the Bank of Canada reduces its policy rate. However, most forecasts suggest only modest decreases rather than sharp drops. Market conditions and economic data will ultimately drive future changes.

What is considered a good mortgage rate in Canada today?

A good mortgage rate in Canada today is typically below the national average for your loan type and term. For example, a 5-year fixed rate under 5% is generally competitive in the current market. Working with a broker can help you access better-than-advertised rates.

Should I choose a fixed or variable mortgage rate in Canada?

Fixed rates are better if you want predictable payments and protection from rate increases. Variable rates can offer savings if interest rates fall, but they come with more risk. Your decision should depend on your financial stability and risk tolerance.

How does the Bank of Canada affect mortgage rates?

The Bank of Canada sets the overnight rate, which influences the prime rate used by lenders. When the central bank raises or lowers rates, variable mortgage rates typically follow. Fixed rates are affected more by bond yields than direct policy changes.

Can I negotiate mortgage interest rates in Canada?

Yes, mortgage rates are often negotiable, especially if you have a strong financial profile. Lenders may offer discounts below posted rates to compete for your business. Comparing multiple lenders or using a broker can improve your chances of getting a better deal.

What is the difference between insured and uninsured mortgage rates?

Insured mortgage rates are usually lower because they are backed by CMHC or another insurer, reducing lender risk. Uninsured mortgages often come with slightly higher rates but offer more flexibility. The difference depends on your down payment and loan structure.