Investing in rental properties can be a game-changer for building long-term wealth in Canada, but understanding cash flow is crucial before taking the plunge. Cash flow rental property Canada investors often overlook is the difference between gross rental income and the total expenses required to operate the property. Without a clear grasp of this, even a seemingly profitable property can become a financial burden. In this guide, we’ll break down how to calculate cash flow, examine real Canadian scenarios, explore essential metrics like cap rate and cash-on-cash return, and provide actionable tips to ensure your rental property generates real profit.

Table of Contents

Cash Flow Rental Property Canada Complete Guide to Profitable Investing

What Is Cash Flow in Rental Property (Canada Explained)

Cash flow refers to the net money you earn from a rental property after all expenses are paid. Positive cash flow means the property generates more income than it costs to operate, while negative cash flow indicates expenses exceed income. Understanding this distinction is essential for Canadian investors aiming for sustainable profits.

Unlike appreciation, which depends on market growth, cash flow provides immediate, tangible returns that can fund future investments or cover unexpected expenses.

Simple Definition of Cash Flow

Simply put, cash flow equals monthly rental income minus all property expenses, including mortgage payments, taxes, insurance, and maintenance. It’s the money that actually hits your bank account.

Positive vs Negative Cash Flow

Positive cash flow is ideal for investors seeking regular income. Negative cash flow might be acceptable if the property’s appreciation potential outweighs short-term losses, but it requires careful planning and capital reserves.

Why Cash Flow Matters in Canadian Real Estate

Canada’s real estate markets, especially Toronto and Vancouver, can have high property prices and taxes. Monitoring cash flow ensures you aren’t overleveraging and helps maintain financial stability despite market fluctuations.

Cash Flow vs Appreciation Strategy

While some investors rely on long-term appreciation, cash flow-focused investors prioritize properties that generate consistent monthly income. Balancing both approaches can maximize returns.

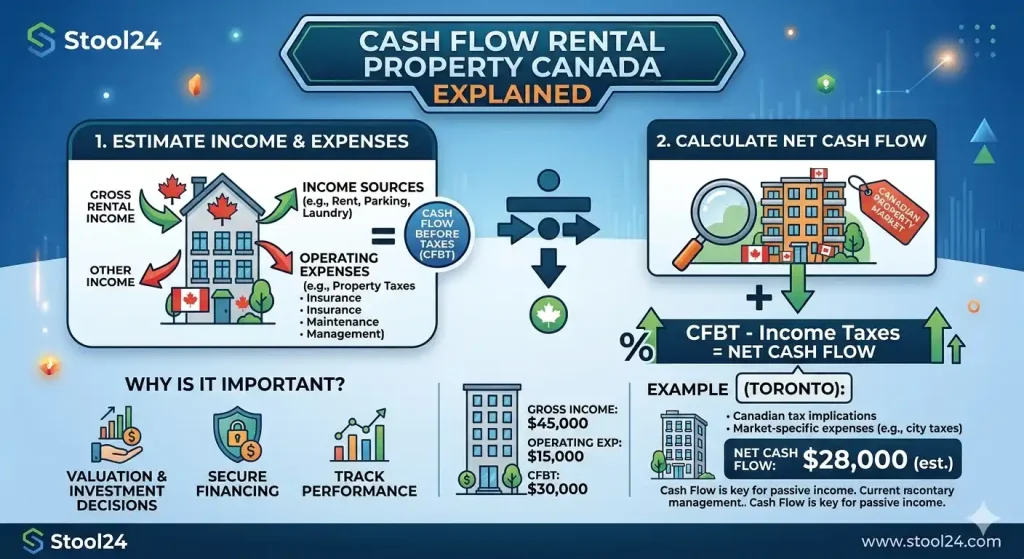

How to Calculate Cash Flow Rental Property Canada

Calculating cash flow starts with gathering accurate income and expense data. Here’s a structured approach for Canadian rental properties.

The Basic Cash Flow Formula

Cash Flow = Total Rental Income – Total Expenses

Expenses include mortgage payments, property taxes, insurance, maintenance, utilities, and property management fees.

Monthly Rental Income Breakdown

Include rent from tenants, parking fees, and any other income streams. Being thorough ensures your calculations reflect reality.

Full Expense Breakdown (Canada-Specific)

- Property taxes

- Mortgage payments

- Insurance

- Maintenance costs

- Property management fees

- Vacancy allowance

Use our rental property calculator to enter your numbers and see monthly cash flow instantly.

Example Calculation (Real Canadian Scenario)

Consider a Toronto condo renting for CAD 2,200 per month. Monthly mortgage is CAD 1,400, taxes are CAD 200, insurance CAD 50, and maintenance CAD 100. Cash flow = 2,200 – (1,400 + 200 + 50 + 100) = CAD 450 positive cash flow.

Cash Flow Rental Property Canada Example (Real Numbers)

Below is a comparison of monthly cash flow across different Canadian markets:

The table shows expected monthly cash flow in three representative cities:

| City | Monthly Rent | Expenses | Cash Flow |

|---|---|---|---|

| Toronto | 2,200 | 1,750 | 450 |

| Calgary | 1,800 | 1,200 | 600 |

| Winnipeg | 1,500 | 950 | 550 |

Key Metrics Beyond Cash Flow (Most Guides Miss This)

Cash flow is important, but other metrics like cap rate, cash-on-cash return, and NOI provide deeper insight.

Cap Rate vs Cash Flow (Important Difference)

Cap rate measures potential return based on property value, while cash flow focuses on actual monthly income. Learn more with our detailed cap rate explanation.

Cash-on-Cash Return Explained

This metric compares annual cash flow to your total cash invested, helping you evaluate true profitability.

Net Operating Income (NOI)

NOI = Rental Income – Operating Expenses (excluding mortgage). It indicates property earning potential before financing costs.

Debt Service Coverage Ratio (DSCR)

DSCR shows how easily income covers debt obligations. Lenders often require a ratio above 1.2 for financing approval.

Can You Still Get Positive Cash Flow in Canada in 2026?

High interest rates and rising property prices make positive cash flow challenging in major cities, but opportunities exist in secondary markets and strategic neighborhoods.

Impact of Interest Rates (Bank of Canada)

Mortgage rates directly affect cash flow. A higher rate increases monthly payments, reducing profit unless rents rise proportionally.

Mortgage Stress Test Rules

Canadian lenders require borrowers to pass stress tests, ensuring you can handle rate increases without negative cash flow.

Best Cities for Cash Flow in Canada

Smaller cities or suburbs often offer higher yields and lower purchase prices. Calgary, Winnipeg, and some Ontario mid-sized cities are examples.

Why Major Cities Are Hard for Cash Flow

High property prices, taxes, and insurance costs often outweigh rental income in Vancouver and Toronto.

How to Find Cash Flow Rental Properties (Step-by-Step)

- Choose the Right Market: Analyze rental demand and price trends.

- Analyze Rent Potential: Check comparable properties for realistic income.

- Estimate All Expenses: Include taxes, insurance, vacancy, and maintenance.

- Run the Numbers: Use a calculator to ensure positive cash flow.

- Apply the 1% Rule: Monthly rent should ideally be ≥1% of purchase price in Canada.

Common Mistakes That Kill Rental Property Cash Flow

- Underestimating operating expenses

- Ignoring vacancy periods

- Overleveraging with high mortgages

- Not stress testing interest rates

- Buying in low-yield markets

Expert Tips to Increase Cash Flow

- Raise rent strategically when market allows

- Add secondary units like basement suites

- Consider short-term rentals in high-demand areas

- Reduce operating costs without compromising quality

- Refinance or optimize mortgage terms

FAQS For Cash Flow Rental Property Canada

What is a good cash flow for a rental property in Canada?

A good cash flow varies by city, but generally, a positive monthly cash flow of CAD 300–500 is considered healthy for Canadian rental properties. Secondary cities like Calgary or Winnipeg often offer higher yields than major markets like Toronto or Vancouver.

How do I calculate cash flow for a rental property in Canada?

Cash flow is calculated by subtracting all property expenses—including mortgage, taxes, insurance, maintenance, and vacancy—from total rental income. You can also use a rental property calculator to simplify this process.

Can rental properties in Toronto or Vancouver generate positive cash flow?

It’s challenging due to high property prices and taxes, but possible in certain neighborhoods or with multi-unit properties. Careful market analysis and precise expense calculation are essential to ensure profitability.

What expenses should I include in cash flow calculations?

Include mortgage payments, property taxes, insurance, maintenance, utilities, property management fees, and a vacancy allowance. Accurately estimating these ensures realistic cash flow projections.

What is the 1% rule in Canada?

The 1% rule suggests that monthly rent should equal at least 1% of the property’s purchase price to generate acceptable cash flow. While more common in secondary markets, it provides a quick benchmark for property evaluation.

Is negative cash flow ever worth it?

Negative cash flow may be acceptable if the property has strong appreciation potential or tax benefits. However, it requires sufficient reserves to cover ongoing costs without financial strain.

How much down payment is needed for a rental property in Canada?

Most lenders require a minimum 20% down payment for Canadian investment properties. Larger down payments can improve cash flow and reduce financing costs over time.

Quick Summary

Cash flow rental property Canada success depends on careful analysis of income, expenses, and market conditions. Focus on realistic calculations, include key metrics like cap rate and cash-on-cash return, and always stress test mortgage scenarios. Secondary cities and thoughtful strategies can ensure positive cash flow and long-term profitability. For Canadian investors looking for precise financial tools, check out our tax toolkit for deeper insights into optimizing rental income and expenses.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is a good cash flow for a rental property in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A good cash flow varies by city, but generally, a positive monthly cash flow of CAD 300–500 is considered healthy for Canadian rental properties. Secondary cities like Calgary or Winnipeg often offer higher yields than major markets like Toronto or Vancouver.” } }, { “@type”: “Question”, “name”: “How do I calculate cash flow for a rental property in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Cash flow is calculated by subtracting all property expenses—including mortgage, taxes, insurance, maintenance, and vacancy—from total rental income. You can also use a rental property calculator to simplify this process.” } }, { “@type”: “Question”, “name”: “Can rental properties in Toronto or Vancouver generate positive cash flow?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “It’s challenging due to high property prices and taxes, but possible in certain neighborhoods or with multi-unit properties. Careful market analysis and precise expense calculation are essential to ensure profitability.” } }, { “@type”: “Question”, “name”: “What expenses should I include in cash flow calculations?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Include mortgage payments, property taxes, insurance, maintenance, utilities, property management fees, and a vacancy allowance. Accurately estimating these ensures realistic cash flow projections.” } }, { “@type”: “Question”, “name”: “What is the 1% rule in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The 1% rule suggests that monthly rent should equal at least 1% of the property’s purchase price to generate acceptable cash flow. While more common in secondary markets, it provides a quick benchmark for property evaluation.” } }, { “@type”: “Question”, “name”: “Is negative cash flow ever worth it?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Negative cash flow may be acceptable if the property has strong appreciation potential or tax benefits. However, it requires sufficient reserves to cover ongoing costs without financial strain.” } }, { “@type”: “Question”, “name”: “How much down payment is needed for a rental property in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Most lenders require a minimum 20% down payment for Canadian investment properties. Larger down payments can improve cash flow and reduce financing costs over time.” } } ] }