A $70,000 salary, rising interest rates, and a modest down payment—this is the reality many Canadians face when trying to buy a home today. Understanding home affordability based on salary Canada isn’t just about guessing a number. It’s about knowing how lenders calculate your limits, what costs you’ll actually pay, and how your lifestyle fits into the equation. In this guide, you’ll learn how affordability really works in Canada, see real salary examples, and discover practical ways to increase your buying power without stretching your budget too thin.

Table of Contents

Home Affordability Based on Salary Canada How Much House Can You Really Afford?

When you ask how much house you can afford, lenders don’t just look at your salary. They evaluate your income, debts, interest rates, and even future financial risks. In Canada, affordability is carefully calculated using strict rules to ensure borrowers can handle payments even if rates rise.

What Home Affordability Means in Canada

Home affordability in Canada refers to how much mortgage you can realistically carry based on your financial situation. Your salary is just one part of the equation. Lenders also consider your monthly expenses, debt obligations, and housing costs.

Owning a home comes with more than just a mortgage payment. A realistic view includes:

- Monthly mortgage payments

- Property taxes

- Home insurance

- Utilities and maintenance

- Unexpected repairs

Gross Income vs Net Income (Why It Matters)

Lenders use gross income (before tax) to calculate affordability. But your real budget depends on net income—what you actually take home. This gap often leads buyers to overestimate what they can afford.

The True Cost of Owning a Home in Canada

According to Canada Mortgage and Housing Corporation, housing costs should remain manageable even during financial stress. That’s why lenders include buffers like insurance and stress testing.

It’s not just about qualifying—it’s about staying financially stable after you move in.

How Home Affordability Based on Salary Canada Is Calculated

Lenders rely on structured formulas to determine how much mortgage you qualify for. These rules are set by regulators like OSFI to reduce financial risk.

The GDS and TDS Ratios Explained

Two key ratios determine affordability:

- GDS (Gross Debt Service): Should be under 39% of your gross income

- TDS (Total Debt Service): Should be under 44% including all debts

These ratios ensure your housing costs don’t overwhelm your finances.

The 30% Rule vs Real Mortgage Rules

The popular “30% rule” suggests spending no more than 30% of income on housing. However, Canadian lenders allow higher ratios due to strict qualification processes.

Comparison of affordability rules:

| Rule | Percentage | Usage |

|---|---|---|

| 30% Rule | 30% | General budgeting guideline |

| GDS Ratio | Up to 39% | Lender qualification |

| TDS Ratio | Up to 44% | Includes all debts |

Mortgage Stress Test (Why It Reduces Your Budget)

The stress test requires you to qualify at a higher interest rate than your actual mortgage rate. The Bank of Canada influences these rates, which directly affect your borrowing power.

As a result, your approved mortgage may be lower than expected.

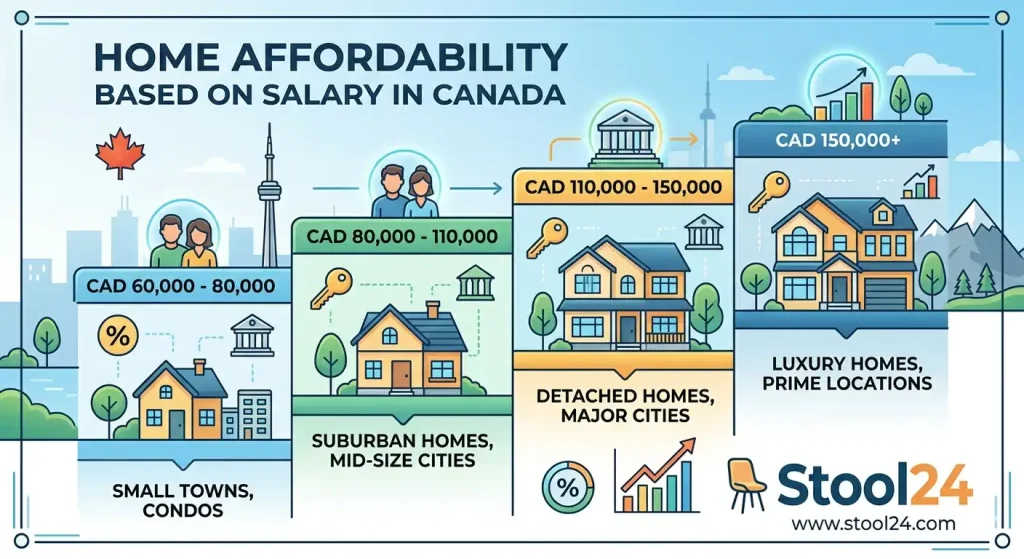

Salary-to-Home Price Examples (Real Canadian Scenarios)

To understand affordability better, let’s look at real salary scenarios. These estimates assume average rates and minimal debt.

This table shows estimated home prices based on salary levels in Canada.

| Salary | Estimated Home Price | Monthly Payment |

|---|---|---|

| $50,000 | $250,000 – $300,000 | $1,200 – $1,500 |

| $70,000 | $350,000 – $420,000 | $1,800 – $2,200 |

| $100,000 | $500,000 – $600,000 | $2,500 – $3,000 |

Example Monthly Budget Breakdown

A $70,000 salary might allow a $2,000 monthly housing budget. After adding taxes and utilities, actual costs could rise to $2,400.

Urban vs Smaller City Affordability Differences

In cities like Toronto or Vancouver, affordability drops significantly. Meanwhile, smaller cities offer more value for the same salary, often increasing purchasing power by 20–40%.

Location can change everything.

Even a small shift in interest rates can change your affordability by thousands. That’s why using tools like the Canadian mortgage calculator helps estimate real monthly payments quickly.

Step-by-Step: Calculate Your Home Affordability

If you want a clearer picture, follow a structured process instead of guessing.

Step 1 – Determine Your Income and Debts

List your gross income and all monthly debt payments, including credit cards and loans.

Step 2 – Estimate Your Down Payment

In Canada, minimum down payments range from 5% to 20%. A larger down payment reduces your mortgage and insurance costs.

Step 3 – Apply GDS/TDS Ratios

Use these ratios to estimate your maximum housing budget.

Step 4 – Factor in Interest Rates

Higher rates reduce affordability. Even a 1% increase can lower your buying power by nearly 10%.

For a quick estimate, try this tool.

[ Check Your Affordability Now ] Mortgage Affordability Calculator Canada

Key Factors That Affect Affordability (Beyond Salary)

Your salary sets the foundation, but several other factors shape your final approval.

Credit Score and Loan Approval

A higher credit score improves your chances of getting better interest rates, which directly increases affordability.

Down Payment Size and CMHC Insurance

If your down payment is under 20%, mortgage insurance is required. You can estimate this using a mortgage insurance cost calculator.

Interest Rates and Loan Term

Longer terms reduce monthly payments but increase total interest paid over time.

Location and Housing Market Conditions

Markets vary widely across Canada. Government programs like the Home Buyers’ Plan can also affect affordability.

Rent vs Buy: What Makes Sense Based on Your Salary?

Deciding between renting and buying depends on your financial stability and long-term goals.

This table compares renting and buying based on salary impact.

| Factor | Renting | Buying |

|---|---|---|

| Monthly Cost | Flexible | Fixed (mortgage) |

| Equity | None | Builds over time |

| Upfront Cost | Low | High (down payment) |

When Renting Is Smarter

If your income is unstable or you lack savings, renting offers flexibility.

When Buying Becomes Affordable

Buying makes sense when your income is stable, debt is low, and you plan to stay long-term.

Long-Term Financial Impact

Over time, owning can build wealth, while renting offers short-term flexibility.

Common Mistakes When Estimating Home Affordability

Many buyers rely on rough estimates instead of accurate calculations.

- Ignoring hidden costs

- Overestimating salary power

- Not considering rate increases

- Skipping stress test calculations

- Relying only on calculators

Smart planning avoids these pitfalls.

Using structured tools like the tax toolkit can help you understand your after-tax income more clearly before committing.

Expert Tips to Improve Your Home Affordability

Improving affordability doesn’t always mean earning more. Small changes can make a big difference.

Increase Your Down Payment Strategically

Saving even an extra 5% can reduce insurance costs and monthly payments.

Reduce Debt Before Applying

Paying off credit cards or loans improves your TDS ratio instantly.

Improve Credit Score Quickly

Pay bills on time and reduce credit utilization to boost your score.

Use Government Programs in Canada

Programs backed by CMHC and federal initiatives can support first-time buyers.

FAQS For Home Affordability Based on Salary Canada

How much house can I afford based on my salary in Canada?

Your affordability depends on your gross income, debts, and current interest rates. Most lenders in Canada use GDS and TDS ratios to determine how much you can borrow. A stable income with low debt can significantly increase your purchasing power.

What salary do I need to buy a $500,000 home in Canada?

Typically, you would need a household income of around $90,000 to $110,000, depending on your down payment and debts. Interest rates and mortgage terms also play a major role in affordability. A larger down payment can lower the income requirement.

Does the 30% rule apply in Canada?

The 30% rule is a general budgeting guideline, but lenders in Canada follow GDS and TDS ratios instead. These allow slightly higher spending depending on your financial situation. It’s better to rely on lender calculations than simple rules.

Do lenders use gross or net income to calculate affordability?

Canadian lenders primarily use gross income (before tax) when assessing mortgage affordability. However, your net income determines your real monthly budget. This is why some buyers feel financially stretched even after approval.

How does the mortgage stress test affect affordability?

The stress test requires borrowers to qualify at a higher interest rate than their actual mortgage rate. This reduces the maximum loan amount you can get approved for. It’s designed to ensure you can handle future rate increases.

How much down payment is required to buy a home in Canada?

The minimum down payment is 5% for homes under $500,000, with higher requirements for more expensive properties. If your down payment is below 20%, mortgage insurance is mandatory. A higher down payment improves affordability and reduces monthly costs.

Can I afford a home in Canada with a $70,000 salary?

Yes, but your affordability depends on your debts, down payment, and location. A $70,000 salary may support a home price between $350,000 and $420,000 under typical conditions. Lower debt and a higher down payment can increase your budget.

Quick Summary

Understanding home affordability based on salary Canada requires more than just income calculations. Lenders use structured rules like GDS, TDS, and stress testing to determine safe borrowing limits. Your affordability depends on income, debt, interest rates, and location. By using accurate tools, planning your budget, and improving key financial factors, you can confidently determine how much home you can truly afford without risking financial strain.