A lender reviews your income, housing costs, and debt before approving a mortgage. One key number often decides everything—the gross debt service ratio Canada. If it’s too high, your approval chances drop quickly.

This guide explains how GDS works, how to calculate it step by step, and how to improve it using practical strategies. You’ll also learn how Canadian lenders like CMHC and major banks evaluate your ratio in real scenarios.

Gross Debt Service Ratio Canada Complete Guide to GDS Calculation & Mortgage Approval

What Is Gross Debt Service Ratio (GDS) in Canada?

The gross debt service ratio measures how much of your gross monthly income goes toward housing costs. Lenders use it to determine if you can realistically afford a mortgage.

In Canada, institutions like CMHC and banks such as RBC or TD rely heavily on this ratio. If your GDS is too high, even a strong credit score may not be enough for approval.

What Counts as Housing Costs in GDS?

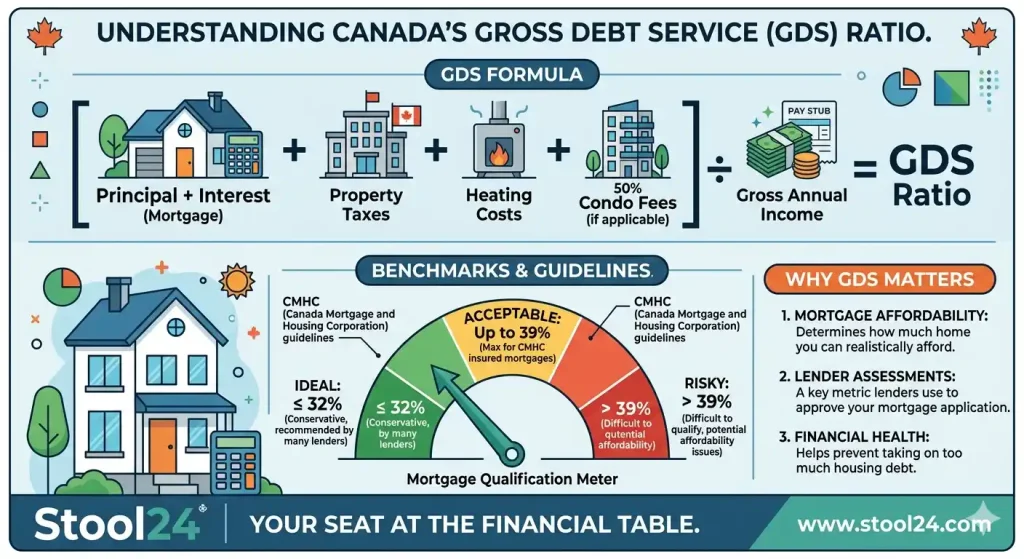

GDS focuses only on housing-related expenses. These are the costs lenders consider when calculating your ratio:

- Mortgage principal and interest

- Property taxes

- Heating costs

- 50% of condo fees (if applicable)

These expenses form the core of your affordability calculation.

What Is NOT Included in GDS?

Unlike total debt ratios, GDS excludes other debts. That means:

- Credit card payments

- Car loans

- Student loans

- Personal loans

Those are included in a separate metric called TDS.

Gross Debt Service Ratio Canada Formula Explained

The formula itself is simple, but understanding each part makes a big difference when planning your mortgage.

GDS Ratio Formula Breakdown

Here’s how lenders calculate it:

GDS = (Total Housing Costs ÷ Gross Monthly Income) × 100

For example, if your monthly income is $6,000 and housing costs are $1,800, your GDS is 30%.

Example Calculation (Step-by-Step)

Let’s break it down into a real-world scenario:

- Monthly income: $5,500

- Mortgage payment: $1,400

- Property tax: $300

- Heating: $150

- Total housing cost: $1,850

- GDS = (1,850 ÷ 5,500) × 100 = 33.6%

This result is slightly above the ideal threshold, which could affect approval.

Quick GDS Calculation Table

This table shows how income impacts your maximum housing budget based on a 32% GDS limit.

| Monthly Income | Max Housing Cost (32%) |

|---|---|

| $4,000 | $1,280 |

| $5,000 | $1,600 |

| $6,000 | $1,920 |

Use this as a quick reference before applying for a mortgage.

What Is a Good Gross Debt Service Ratio in Canada?

A good GDS ratio depends on the lender, but standard benchmarks exist across Canada.

CMHC GDS Guidelines

According to Canada Mortgage and Housing Corporation (CMHC), the recommended GDS ratio is:

- Maximum: 32% for insured mortgages

This limit helps reduce risk for both borrowers and lenders.

Bank vs Alternative Lender Limits

This table compares GDS limits across different lender types in Canada.

| Lender Type | Typical GDS Limit |

|---|---|

| Major Banks (A Lenders) | 32%–35% |

| B Lenders | 35%–39% |

| Private Lenders | Flexible (case-based) |

Private lenders may accept higher ratios, but interest rates are usually higher.

How the Mortgage Stress Test Affects GDS

The mortgage stress test requires borrowers to qualify at a higher interest rate. This rule is enforced by the Office of the Superintendent of Financial Institutions (OSFI).

Even if your actual payment is affordable, the stress test increases your calculated GDS. That’s why many applicants get declined despite manageable real payments.

It’s often the hidden reason behind mortgage rejections.

This is where careful planning becomes critical. If you adjust your loan amount or increase your down payment slightly, you can often bring your GDS back within acceptable limits and pass the stress test more easily.

Gross Debt Service Ratio vs Total Debt Service Ratio (GDS vs TDS)

Understanding the difference helps you avoid confusion during mortgage applications.

Key Differences Explained

This table shows the difference between GDS and TDS ratios.

| Factor | GDS | TDS |

|---|---|---|

| Includes housing costs | Yes | Yes |

| Includes other debts | No | Yes |

| Typical limit | 32%–35% | 40%–44% |

Why Lenders Use Both Ratios

GDS focuses on housing affordability, while TDS looks at your total financial burden. Together, they give lenders a full picture of your risk level.

Which Ratio Matters More for Approval?

Both matter, but GDS is often the first filter. If your housing costs alone are too high, lenders may not even evaluate your full debt profile.

Real-Life Examples of GDS in Canada

Seeing how GDS works in real scenarios helps you understand its impact better.

First-Time Homebuyer Scenario

A buyer earning $4,500 monthly aims to purchase a condo. Their housing costs total $1,300, resulting in a GDS of 28.8%. This falls well within CMHC guidelines.

High-Income but High-Cost City Scenario

In cities like Toronto or Vancouver, even high earners struggle. A $9,000 income with $3,500 housing costs leads to a GDS near 39%, pushing the limits.

Low Income with Low Debt Scenario

A borrower with modest income but minimal expenses may still qualify easily due to a lower GDS, showing that balance matters more than income alone.

How to Improve Your Gross Debt Service Ratio

If your GDS is too high, there are practical ways to improve it before applying.

Increase Your Income Strategically

Adding a co-borrower or including stable bonuses can improve your ratio significantly.

Reduce Housing Costs

Consider a smaller property or increase your down payment. You can explore minimum requirements using the minimum down payment guide.

Optimize Mortgage Structure

Choosing a longer amortization or lower interest rate can reduce monthly payments.

Timing Your Application for Better Approval

Applying after paying down debts or receiving a salary increase can make a noticeable difference.

To get a clearer estimate of your affordability:

[ Calculate Your Mortgage Affordability Now ]

Use this mortgage affordability calculator

Common Mistakes That Hurt Your GDS Ratio

Small missteps can push your ratio above acceptable limits.

Miscalculating Income

Using net income instead of gross income leads to inaccurate results.

Ignoring Hidden Costs

Heating and property taxes are often underestimated but play a key role.

Confusing GDS with TDS

Many borrowers mix the two, which can lead to incorrect expectations.

Overestimating Affordability

Just because you can make payments doesn’t mean lenders will approve them.

Expert Tips to Qualify for a Mortgage in Canada

Smart preparation can improve your chances significantly.

Work with Mortgage Brokers

Brokers understand lender flexibility and can match you with the right option.

Understand Lender Flexibility

Some lenders allow slightly higher GDS if other factors are strong.

Use Pre-Approval Strategically

A pre-approval helps you understand limits before house hunting. You can also estimate payments with a Canadian mortgage calculator.

For deeper financial planning tools, you can also explore the tax toolkit to manage income and affordability more effectively.

Quick Summary

The gross debt service ratio Canada is one of the most important metrics lenders use to assess mortgage affordability. Staying within the 32%–35% range improves your approval chances significantly.

By understanding how to calculate GDS, adjusting your housing costs, and planning strategically, you can position yourself for a stronger mortgage application and better financial stability.

FAQS For Gross Debt Service Ratio Canada

What is a good gross debt service ratio in Canada?

A good gross debt service ratio in Canada is typically 32% or lower for insured mortgages. Some lenders may allow up to 35% or slightly higher depending on your financial profile. Staying below this range improves your chances of mortgage approval.

How do you calculate gross debt service ratio in Canada?

You calculate GDS by dividing your total monthly housing costs by your gross monthly income, then multiplying by 100. Housing costs include mortgage payments, property taxes, heating, and part of condo fees. Using a calculator can simplify this process and reduce errors.

What expenses are included in the gross debt service ratio?

GDS includes mortgage principal and interest, property taxes, heating costs, and 50% of condo fees if applicable. It focuses only on housing-related expenses. Other debts like credit cards or loans are not included.

Can you get a mortgage with a high GDS ratio in Canada?

Yes, but it depends on the lender. Traditional banks have stricter limits, while B lenders or private lenders may accept higher GDS ratios. However, higher ratios often come with higher interest rates and stricter terms.

How does the mortgage stress test affect GDS ratio?

The stress test requires borrowers to qualify at a higher interest rate than their actual mortgage rate. This increases your calculated housing costs, which raises your GDS ratio. As a result, some borrowers may qualify for less than expected.

What is the difference between GDS and TDS in Canada?

GDS measures only housing costs relative to income, while TDS includes all debts such as credit cards and loans. Lenders use both ratios to assess affordability and risk. GDS is usually the first filter during mortgage approval.

How can I lower my gross debt service ratio quickly?

You can lower your GDS by increasing your income, reducing housing costs, or making a larger down payment. Choosing a longer amortization period can also reduce monthly payments. Even small adjustments can significantly improve your ratio.