Imagine needing quick cash for an emergency or a large purchase. If your savings sit inside a Tax-Free Savings Account, understanding tfsa withdrawal rules canada becomes essential before moving any money. Withdrawals are flexible, but contribution room and recontribution timing can create confusion for many Canadians.

This guide explains how TFSA withdrawals actually work, whether they are taxed, and how they affect your future contribution room. You will also learn practical strategies, common mistakes, and real examples so you can withdraw money without triggering penalties or losing valuable tax-free growth.

Table of Contents

TFSA Withdrawal Rules Canada: Complete Guide to Tax-Free Withdrawals and Contribution Room

A TFSA is one of the most flexible investment accounts available to Canadians. Unlike some retirement plans, you can withdraw funds at any time. The key detail is understanding how those withdrawals interact with contribution limits and future deposits.

According to guidance from the Canada Revenue Agency TFSA program overview, withdrawals are generally tax-free. However, recontributing the same amount too soon can cause an over-contribution penalty.

Understanding TFSA Withdrawal Rules in Canada

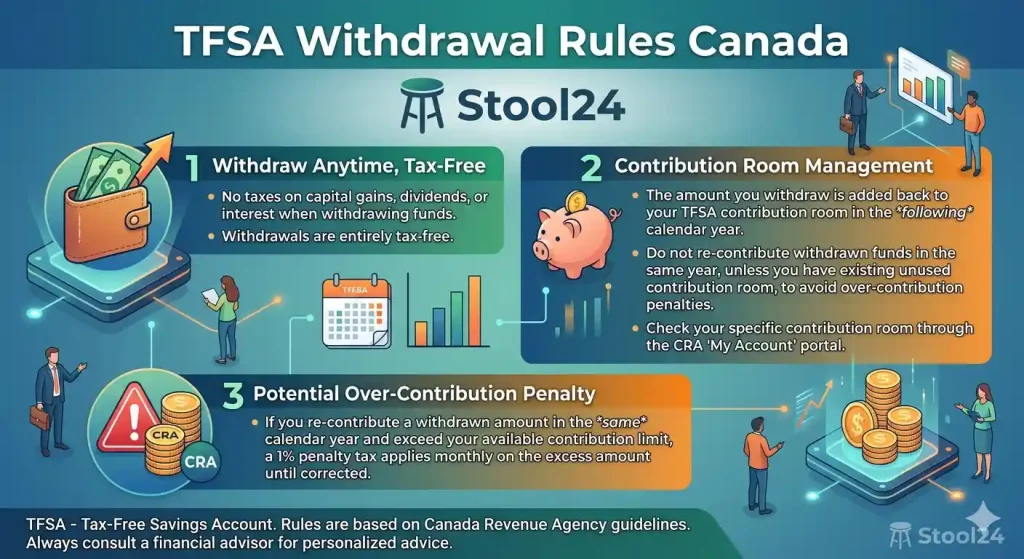

Most people ask a simple question first: can you take money out whenever you want? In almost all cases, the answer is yes. A TFSA allows withdrawals at any time without triggering income tax.

This flexibility makes the account useful for both long-term investing and short-term savings goals.

What Is a TFSA and How Withdrawals Work

A Tax-Free Savings Account is a registered account created by the federal government in 2009. Investment income inside the account grows tax-free, and withdrawals do not count as taxable income.

Financial institutions such as banks and brokerages administer these accounts, but the contribution limits and rules are set by the federal government.

Financial institutions such as banks and brokerages administer these accounts, but the contribution limits and rules are set by the federal government.

Are TFSA Withdrawals Taxable in Canada?

No. Withdrawals from a TFSA are not taxed. The money you take out will not appear as income on your tax return.

Government benefits such as Old Age Security or the Canada Child Benefit also remain unaffected by TFSA withdrawals. This is a major advantage compared with other retirement accounts.

Key TFSA Withdrawal Rules Every Canadian Should Know

Before withdrawing funds, keep these core rules in mind.

- Withdrawals are completely tax-free.

- The withdrawn amount is added back to your contribution room the following year.

- Re-contributing too early may trigger an excess contribution penalty.

- You can withdraw investments or cash depending on your account structure.

In short, flexibility is high—but timing matters.

How TFSA Withdrawals Affect Contribution Room

Contribution room is where many Canadians become confused. Taking money out does not immediately increase your room for the current year.

The withdrawn amount returns to your available contribution room on January 1 of the next calendar year.

How Contribution Room Is Calculated

Every year the federal government sets a new TFSA contribution limit. For example, the annual limit reached $7,000 in 2024 according to data published by the Canada Revenue Agency contribution guidelines.

If you withdraw money during the year, that amount is tracked separately and restored to your limit the following year.

When Withdrawn Amounts Are Added Back

The timeline works like this. If you withdraw $5,000 in July 2025, that $5,000 becomes available again on January 1, 2026.

This delayed reset is designed to prevent people from repeatedly withdrawing and depositing funds within the same year.

Example: TFSA Withdrawal and Contribution Room Timeline

The table below illustrates how withdrawals affect future contribution room.

| TFSA Contribution Room Example | Contribution | Withdrawal | Available Room |

|---|---|---|---|

| 2025 | $7,000 | $3,000 | $4,000 remaining |

| 2026 | $7,000 new limit | $3,000 restored | $10,000 total |

Understanding this timeline prevents accidental over-contributions.

TFSA Withdrawal Rules Canada: When You Can Re-Contribute

The recontribution rule is the most important detail within the tfsa withdrawal rules canada framework.

You can add the withdrawn amount back—but the timing determines whether it counts as a new contribution.

Re-Contributing in the Same Year (Risk of Over-Contribution)

If you withdraw $5,000 and deposit the same amount again during the same calendar year, the CRA counts that as a new contribution.

If you already used your annual contribution limit, this may create an excess contribution.

Re-Contributing the Next Calendar Year

Waiting until the next year resets the rules. The withdrawn amount is added to your available room automatically.

This is why some investors withdraw funds late in December when they plan to recontribute early the following year.

Penalty for Over-Contributing to a TFSA

The CRA imposes a penalty if you exceed your limit.

That penalty is 1% per month on the excess amount until it is removed, as explained in official CRA guidance.

Small mistakes can become expensive if they continue for several months.

How to Withdraw Money From Your TFSA (Step-by-Step)

Withdrawing money is usually simple. Each financial institution has its own process, but the general steps are similar.

Step 1 — Contact Your Financial Institution

Start by logging into your brokerage or banking platform. Most institutions allow withdrawals online.

You can also call the institution directly if the account holds complex investments.

Step 2 — Choose Withdrawal Method

Common withdrawal methods include:

- Cash withdrawal to a bank account

- Selling investments inside the TFSA

- Transferring funds between accounts

Some withdrawals may take several business days depending on the investment type.

Step 3 — Track Your Contribution Room

Always track your TFSA contribution history carefully.

The CRA My Account portal provides estimates, but financial planners often recommend keeping your own records.

Many Canadians simplify this by using tools from the tax toolkit to monitor contributions and withdrawals.

Sometimes the easiest way to understand TFSA growth is simply running the numbers.

A quick estimate using a calculator can reveal how much long-term growth you might lose after withdrawing funds. [ Use the TFSA Growth Calculator ]

See how withdrawals and contributions affect future savings using the TFSA growth calculator guide. You can also learn how compounding works inside a TFSA in this detailed explanation of how TFSA growth works.

Real Examples of TFSA Withdrawal Scenarios

Rules become easier to understand when you look at real-life examples.

Scenario 1: Emergency Withdrawal

Suppose you withdraw $4,000 for a home repair in May. The money is tax-free, and your TFSA balance simply decreases.

However, that $4,000 will not be available for recontribution until the following January.

Scenario 2: Withdrawing and Re-Contributing the Same Year

A person withdraws $6,000 in June but later redeposits the same amount in August.

If their annual contribution room was already used, the redeposit becomes an over-contribution.

Scenario 3: Year-End Withdrawal Strategy

Some investors withdraw funds near the end of December.

Because the contribution room resets on January 1, they can redeposit the same amount almost immediately.

This technique can help rebalance investments or move money between institutions.

Special TFSA Withdrawal Situations

Some situations involve slightly different rules, especially for non-residents or account transfers.

TFSA Withdrawals for Non-Residents

Non-residents of Canada can still withdraw money from a TFSA. Withdrawals remain tax-free.

However, new contributions made while living outside Canada may face additional penalties.

Does Withdrawing Affect Government Benefits?

No. TFSA withdrawals do not count as taxable income.

This means they typically do not affect federal programs such as Old Age Security or the Guaranteed Income Supplement.

TFSA Transfer vs Withdrawal

The table below shows the difference between transferring and withdrawing funds.

| TFSA Transfer vs Withdrawal Comparison | TFSA Transfer | TFSA Withdrawal |

|---|---|---|

| Tax impact | None | None |

| Contribution room effect | No change | Restored next year |

| Best use | Moving accounts | Accessing cash |

Transfers usually make more sense if you simply want to move investments to another institution.

Common TFSA Withdrawal Mistakes Canadians Make

Several common mistakes appear again and again among TFSA users.

- Re-contributing the withdrawn amount too early

- Ignoring contribution tracking

- Withdrawing instead of transferring between accounts

- Assuming contribution room resets immediately

Even experienced investors occasionally misunderstand the recontribution rule.

Expert Tips for Managing TFSA Withdrawals

Financial planners often suggest treating the TFSA as a long-term growth account whenever possible.

Statistics from the Department of Finance Canada show that millions of Canadians now hold TFSA accounts, with assets exceeding hundreds of billions nationally.

Because of this massive growth potential, unnecessary withdrawals can slow compounding returns.

Pros

- Tax-free withdrawals

- No effect on benefits

- Flexible access to savings

Cons

- Contribution room recovery takes time

- Over-contribution penalties can occur

- Withdrawals reduce long-term growth

The smartest strategy is usually simple: withdraw only when necessary and track your contribution room carefully.

FAQS For TFSA Withdrawal Rules Canada

Can I withdraw money from my TFSA anytime in Canada?

Yes. Under TFSA withdrawal rules in Canada, you can withdraw funds at any time without paying tax. Most banks and investment platforms allow withdrawals online, although selling investments may take a few business days before the money becomes available.

Do TFSA withdrawals count as income in Canada?

No. TFSA withdrawals are not considered taxable income and do not appear on your tax return. Because of this, they typically do not affect government benefits such as Old Age Security or the Canada Child Benefit.

When can I re-contribute money after a TFSA withdrawal?

You can re-contribute the withdrawn amount starting January 1 of the following year. If you re-deposit the same amount during the same calendar year without available contribution room, the CRA may treat it as an excess contribution.

What happens if I re-contribute too early after withdrawing from my TFSA?

Re-contributing before your contribution room resets can trigger an over-contribution penalty. The Canada Revenue Agency applies a 1% monthly tax on the excess amount until it is removed from the account.

Does withdrawing from a TFSA increase contribution room?

Yes, but not immediately. The amount you withdraw is added back to your TFSA contribution room at the start of the next calendar year. This allows you to replace the withdrawn funds later without losing contribution space.

Is it better to transfer or withdraw money from a TFSA?

If you want to move investments between financial institutions, a direct TFSA transfer is usually better. Transfers do not affect contribution room, while withdrawals temporarily reduce available contribution space until the next year.

Can non-residents withdraw money from a TFSA?

Yes. Non-residents can withdraw money from their TFSA without paying Canadian tax on the withdrawal. However, making new contributions while living outside Canada may trigger additional penalties.

Quick Summary

The tfsa withdrawal rules canada system offers remarkable flexibility. You can withdraw funds anytime without paying tax, which makes the TFSA ideal for both emergency savings and long-term investing.

The critical rule to remember is timing. Withdrawals restore contribution room in the following calendar year, not immediately. Re-contributing too soon can trigger a 1% monthly penalty.

By tracking your contribution room, using reliable tools like the tax toolkit, and understanding recontribution timing, you can use your TFSA strategically while protecting its powerful tax-free growth.