A couple earning $85,000 a year applies for a mortgage. Their monthly debts look manageable, yet the lender still says their debt ratio is high. What happened? The answer often lies in understanding gross vs net income for DTI. Mortgage lenders usually evaluate income before taxes when calculating debt-to-income ratios, which can significantly affect borrowing capacity.

This guide explains how gross and net income affect your Debt-to-Income ratio in Canada. You’ll learn why lenders rely on gross income, how DTI is calculated, and how Canadian mortgage rules like GDS and TDS ratios influence approval decisions. By the end, you’ll know exactly how lenders assess your financial profile and how to improve your numbers before applying for a loan.

Table of Contents

Gross vs Net Income for DTI Which Income Do Lenders Use in Canada?

When lenders review your mortgage or loan application, they calculate a debt-to-income ratio to determine whether you can handle additional payments. This is where the discussion of gross vs net income for DTI becomes critical.

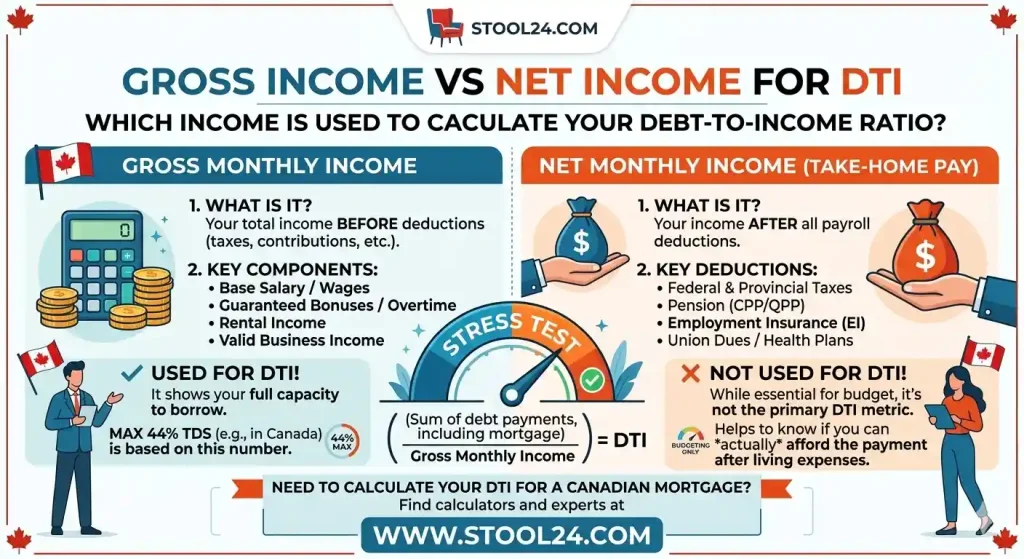

In most cases, Canadian lenders use gross income, which is your earnings before tax deductions. Net income—also called take-home pay—shows what actually lands in your bank account. While both numbers matter for personal budgeting, lenders prefer gross income because it provides a consistent measure for evaluating borrowers.

Understanding Debt-to-Income (DTI) Ratio

Your debt-to-income ratio measures how much of your income goes toward debt payments. Lenders use it to estimate the risk of approving a loan or mortgage.

Put simply, DTI compares your monthly debt obligations with your monthly income. A lower ratio means you have more income available to handle new payments.

What Is a Debt-to-Income Ratio?

The debt-to-income ratio represents the percentage of your income used to pay recurring debts each month. These typically include:

- Mortgage or rent payments

- Car loans

- Credit card minimum payments

- Student loans

- Personal loans

If your monthly debts total $2,000 and your gross monthly income is $6,000, your DTI ratio is about 33%.

Why Lenders Use DTI to Evaluate Borrowers

DTI helps lenders predict whether borrowers can manage additional financial obligations. Banks want reassurance that mortgage payments will not stretch a borrower’s finances too far.

Major Canadian lenders such as Royal Bank of Canada and TD Bank Group commonly use DTI-related metrics during mortgage evaluations.

DTI vs Canadian Debt Service Ratios (GDS and TDS)

Canada relies heavily on two related ratios: Gross Debt Service (GDS) and Total Debt Service (TDS). These standards are widely referenced by the Canada Mortgage and Housing Corporation.

According to guidance from Canada Mortgage and Housing Corporation mortgage affordability guidelines, most borrowers should keep:

- GDS under about 39%

- TDS under about 44%

These ratios are similar to DTI and help lenders assess mortgage affordability.

Gross vs Net Income for DTI: Key Differences

Understanding the difference between gross and net income is essential before calculating any debt ratio.

What Is Gross Income?

Gross income is the total amount you earn before deductions. This includes salary, bonuses, commissions, and sometimes rental or investment income.

Employers usually report gross income on tax forms and pay stubs, making it easy for lenders to verify.

What Is Net Income?

Net income refers to the money left after taxes, pension contributions, and other deductions.

This is the amount you actually receive in your bank account each pay period. For personal budgeting, net income often feels more realistic.

Why Lenders Use Gross vs Net Income for DTI

Lenders rely on gross income because tax rates vary widely between borrowers. Using net income would make comparisons inconsistent.

Financial regulators such as the Office of the Superintendent of Financial Institutions encourage lenders to apply standardized methods when assessing borrower risk.

Gross income offers a simple and consistent metric.

It allows lenders to compare applications fairly, even when tax deductions or benefits differ between households.

The following table highlights the key differences.

Comparison of Gross vs Net Income in Debt-to-Income Calculations

| Feature | Gross Income | Net Income |

|---|---|---|

| Definition | Income before taxes and deductions | Income after taxes and deductions |

| Used for DTI | Yes | Rarely |

| Consistency for lenders | High | Lower |

| Budgeting usefulness | Moderate | Very useful |

How Lenders Calculate DTI Using Gross Income

Once lenders confirm income sources, they calculate DTI using a straightforward formula.

DTI Calculation Formula

The basic formula is simple:

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income

Multiply the result by 100 to convert it into a percentage.

Step-by-Step Example of a DTI Calculation

Here is a simplified example showing how lenders evaluate a borrower.

- Gross monthly income: $6,500

- Mortgage payment estimate: $1,800

- Car loan: $350

- Credit card minimum: $150

- Total monthly debts: $2,300

The DTI ratio becomes:

$2,300 ÷ $6,500 = 0.35 or 35%

This ratio generally falls within acceptable mortgage limits.

If you want a quick way to calculate your numbers, try this tool.

Use a calculator to instantly estimate your ratio based on income and debts.

[ Calculate Your DTI Ratio ] Debt to Income Ratio Calculator Canada

You can also explore a deeper explanation of mortgage approval requirements in this guide on DTI for mortgage approval.

What Debts Are Included in DTI Calculations

Not every expense counts toward DTI, but lenders focus on recurring debts that affect your financial obligations.

Housing Costs Considered in DTI

Mortgage lenders include housing-related costs such as:

- Mortgage payments

- Property taxes

- Heating costs

- Condo fees (if applicable)

Consumer Debts That Count Toward DTI

The following debts typically count in DTI calculations:

- Auto loans

- Credit card minimum payments

- Student loan payments

- Lines of credit

These obligations are considered ongoing financial commitments.

Even small monthly payments can increase your ratio.

Debts That Usually Do Not Count

Some expenses are excluded because they are not long-term debt obligations.

- Groceries

- Utilities

- Insurance premiums

- Mobile phone bills

Canadian Mortgage Rules That Affect DTI

Canada uses a slightly different system than the traditional DTI approach used in the United States.

Lenders rely on GDS and TDS ratios when evaluating mortgage affordability.

Gross Debt Service (GDS) Ratio Explained

GDS measures housing costs relative to gross income.

This includes mortgage payments, property taxes, heating costs, and half of condo fees.

Total Debt Service (TDS) Ratio Explained

TDS expands the calculation by including all other debts.

Most lenders prefer TDS ratios below 44%, though exact thresholds vary.

Mortgage regulations and stress testing guidelines are monitored by Office of the Superintendent of Financial Institutions mortgage stress test policies.

How the Mortgage Stress Test Affects Borrowers

The Canadian mortgage stress test ensures borrowers could still afford payments if interest rates rise.

This rule has been a major factor in mortgage approvals since 2018.

Because of this policy, many borrowers qualify for smaller mortgage amounts than expected.

Common Mistakes When Using Gross vs Net Income for DTI

Even financially responsible borrowers sometimes misunderstand how lenders calculate ratios.

Using Take-Home Pay Instead of Gross Income

Many borrowers mistakenly calculate DTI using net income. This makes the ratio appear higher than lenders will calculate.

Always start with gross monthly earnings.

Forgetting Certain Monthly Debts

Applicants often overlook credit card minimum payments or lines of credit.

These obligations still count toward debt service ratios.

Overestimating Mortgage Affordability

Another common mistake is assuming lenders evaluate only mortgage payments.

In reality, property taxes, heating costs, and other housing expenses are included.

Expert Tips to Improve Your DTI Ratio

If your debt ratio is too high, several practical strategies can improve it before applying for a mortgage.

Reduce Monthly Debt Obligations

Paying down high-interest credit cards is one of the fastest ways to lower DTI.

Even reducing balances slightly can improve your ratio.

Increase Verified Income

Additional verified income—such as consistent freelance work or rental income—may strengthen a mortgage application.

Lenders typically require documentation for these sources.

Prepare Financial Documents Early

Before applying, gather documents such as pay stubs, tax returns, and bank statements.

This helps lenders verify income quickly and reduces approval delays.

Helpful resources like the tax toolkit can simplify financial preparation before applying for loans or filing taxes.

FAQS For Gross vs Net Income for DTI

Do lenders use gross or net income for DTI in Canada?

Most Canadian lenders calculate debt-to-income ratios using gross income, which is your earnings before taxes and deductions. This provides a standardized way to compare borrowers regardless of tax situations. Net income may still be reviewed during budgeting discussions, but it is rarely used for official DTI calculations.

Why is gross income used instead of net income for DTI?

Lenders prefer gross income because tax rates, deductions, and benefits vary widely between individuals. Using pre-tax income creates a consistent metric for evaluating mortgage risk. This approach also aligns with Canadian mortgage guidelines used by banks and insurers.

What is considered a good DTI ratio in Canada?

In Canada, lenders typically evaluate debt ratios using GDS and TDS limits rather than traditional DTI alone. Generally, a Gross Debt Service ratio under 39% and a Total Debt Service ratio under 44% is considered acceptable. Lower ratios increase your chances of mortgage approval.

What debts are included when calculating DTI?

DTI calculations usually include mortgage payments, car loans, credit card minimum payments, student loans, and lines of credit. These are recurring obligations that affect your ability to repay new debt. Everyday expenses like groceries, utilities, and insurance are usually excluded.

Does the mortgage stress test affect DTI calculations in Canada?

Yes, the Canadian mortgage stress test indirectly affects your debt ratios. Lenders calculate your mortgage payments using a higher qualifying interest rate to ensure you could handle future rate increases. This can increase your calculated debt ratio and reduce the mortgage amount you qualify for.

Can self-employed income be used for DTI calculations?

Yes, self-employed borrowers can use their income for DTI calculations, but lenders usually require more documentation. Most banks review two years of tax returns and financial statements to confirm stable earnings. Only verified and consistent income is typically included in the calculation.

How can I lower my DTI ratio before applying for a mortgage?

The fastest way to reduce your DTI ratio is to pay down high-interest debts such as credit cards or personal loans. Increasing your verified income or consolidating debts can also help improve the ratio. Even small reductions in monthly obligations can make a noticeable difference.

Quick Summary

Understanding gross vs net income for DTI is essential when applying for a mortgage in Canada. Lenders typically use gross income because it offers a consistent way to compare borrowers.

- DTI compares monthly debt payments to gross monthly income.

- Canadian lenders rely on GDS and TDS ratios for mortgage qualification.

- Gross income is used because tax deductions vary between borrowers.

- Reducing debt and increasing verified income can improve approval chances.

Before applying for a mortgage, calculate your DTI ratio and review your debts carefully. Small improvements in your financial profile can significantly increase your chances of approval.