A household earning $7,000 a month may feel ready to buy a home. Yet mortgage approval depends on more than income alone. Lenders closely examine your debt-to-income ratio to decide whether your budget can handle a mortgage payment. In Canada, this evaluation uses specific debt service ratios rather than the traditional DTI formula used in other countries.

Expert insight: Canadian lenders follow strict underwriting standards influenced by federal guidelines and mortgage insurers. Understanding how ratios like GDS and TDS work before applying can significantly improve your approval chances and prevent costly rejections.

If you’re researching dti for mortgage approval canada, the goal is simple: understand how lenders calculate affordability and what limits they accept. This guide explains the real thresholds, how to calculate your ratios step by step, and practical ways to improve approval chances before applying.

Table of Contents

DTI for Mortgage Approval Canada Debt-to-Income Rules, Limits, and How to Qualify

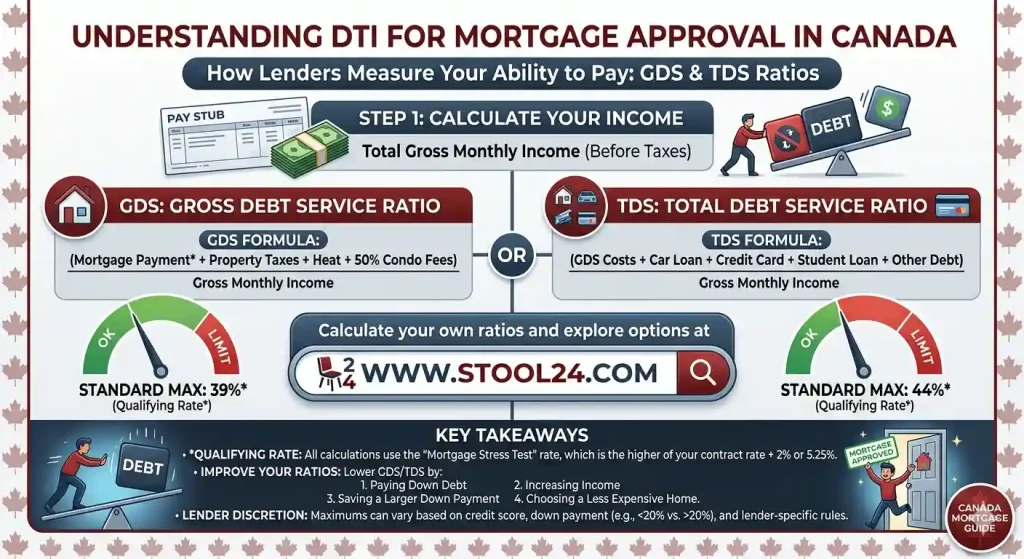

Mortgage lenders want to confirm that borrowers can comfortably manage housing payments alongside existing debt. That’s why the concept behind dti for mortgage approval canada revolves around two ratios used by banks and mortgage insurers: Gross Debt Service (GDS) and Total Debt Service (TDS).

These ratios help lenders determine if a borrower’s income can realistically support a mortgage. If the numbers exceed recommended thresholds, approval becomes harder or the loan amount may shrink.

Understanding DTI for Mortgage Approval in Canada

Many borrowers assume lenders simply compare monthly debt payments to income. In Canada, the system is slightly different. Financial institutions evaluate affordability through specific debt service ratios designed for mortgage lending.

What Is Debt-to-Income Ratio (DTI)?

Debt-to-income ratio measures how much of your income goes toward debt payments. The calculation includes obligations such as credit cards, car loans, and student loans compared with your gross monthly income.

A lower ratio suggests stronger financial stability. Lenders view borrowers with manageable debt levels as less risky.

Why Canada Uses GDS and TDS Instead of Traditional DTI

Canadian mortgage underwriting uses two standardized metrics:

- Gross Debt Service (GDS) – percentage of income spent on housing costs.

- Total Debt Service (TDS) – percentage of income spent on housing plus all other debts.

These ratios are widely used by lenders and mortgage insurers such as the Canada Mortgage and Housing Corporation, which sets national guidelines for insured mortgages.

How Debt Ratios Affect Mortgage Approval Decisions

When reviewing applications, lenders calculate both ratios before approving a mortgage amount. If the ratios exceed recommended limits, the borrower may need to reduce debt or increase income.

Mortgage insurers typically prefer applicants whose financial ratios stay within established limits to minimize lending risk.

Debt-to-Income Limits for Mortgage Approval Canada

One of the most common questions buyers ask is how much debt is acceptable when applying for a mortgage. The limits used across Canadian lenders are fairly consistent.

The following table explains the common thresholds used by mortgage lenders.

| Mortgage Debt Ratio Limits Used by Canadian Lenders | Maximum Recommended Level | What It Includes |

|---|---|---|

| Gross Debt Service (GDS) | 39% | Mortgage payment, property tax, heating, half of condo fees |

| Total Debt Service (TDS) | 44% | Housing costs plus all other debts |

These benchmarks are widely referenced by organizations such as the Financial Consumer Agency of Canada and mortgage insurers.

How to Read These Mortgage Ratio Limits

These limits are not just numbers — they directly affect how much home you can afford:

- Below 35% GDS: Strong application, higher approval chances

- 35%–39% GDS: Acceptable but may require strong credit

- 40%+ GDS: Higher risk, possible rejection

- Below 40% TDS: Ideal borrower profile

- 40%–44% TDS: Borderline approval zone

- Above 44% TDS: Typically declined by lenders

Staying below these thresholds gives lenders confidence that you can manage payments even if interest rates increase.

Maximum DTI for Mortgage Approval Canada

While 39% and 44% are the official thresholds, lenders may set slightly lower targets. Some banks aim for safer ranges such as 35% GDS or 42% TDS depending on the borrower profile.

Borrowers with strong credit scores and stable income may still qualify even when ratios are slightly higher.

Ideal Debt-to-Income Ratio to Get Approved Easily

Mortgage brokers often suggest keeping your TDS ratio under 40% if possible. This improves approval odds and may allow borrowers to qualify for a larger mortgage amount.

Lower ratios also make it easier to pass the mortgage stress test required for most Canadian home loans.

To maximize approval chances and secure better interest rates, aim for:

- GDS ratio under 35%

- TDS ratio under 40%

Borrowers in this range are often considered low-risk and may qualify for better mortgage terms, including lower interest rates and higher borrowing limits.

Lenders also evaluate how close you are to the limit. Even a small reduction in monthly debt can significantly improve your approval outcome.

Differences Between Insured and Uninsured Mortgages

Mortgages with less than 20% down payment require insurance from providers like CMHC, Sagen, or Canada Guaranty. Insured mortgages typically follow stricter ratio guidelines.

Uninsured mortgages may allow slightly more flexibility, though lenders still evaluate affordability carefully.

How Canadian Lenders Calculate Your Debt-to-Income Ratio

Understanding the exact formulas helps buyers estimate their approval chances before speaking with a lender.

Gross Debt Service (GDS) Ratio Formula

The GDS ratio measures how much of your income covers housing expenses.

Formula:

Housing Costs ÷ Gross Monthly Income × 100

Housing costs include mortgage payments, property taxes, heating, and half of condo fees.

Total Debt Service (TDS) Ratio Formula

TDS expands the calculation by including all monthly debts.

(Housing Costs + Other Debt Payments) ÷ Gross Monthly Income × 100

This gives lenders a complete picture of a borrower’s financial obligations.

What Debts Count Toward Mortgage Approval

Most lenders include these obligations when calculating TDS:

- Credit card minimum payments

- Car loans or leases

- Student loans

- Personal loans

- Lines of credit

Even small recurring debts can raise the ratio and affect mortgage approval.

Step-by-Step Example: Calculating DTI for Mortgage Approval Canada

Let’s look at a simplified example to see how lenders calculate these ratios.

The table below illustrates a basic mortgage affordability scenario.

| Example Monthly Financial Situation | Amount |

|---|---|

| Gross household income | $7,000 |

| Mortgage payment | $2,000 |

| Property tax | $300 |

| Car loan | $450 |

| Credit card payments | $150 |

Step-by-Step GDS Calculation

Total housing costs equal $2,300 per month.

GDS = 2,300 ÷ 7,000 = 32.8%

This falls comfortably within the recommended 39% limit.

Step-by-Step TDS Calculation

Total debt obligations equal $2,900.

TDS = 2,900 ÷ 7,000 = 41.4%

The ratio remains within the common 44% threshold used by many lenders.

If you want to check your numbers quickly, try this debt-to-income calculator.

GDS vs TDS: Key Differences Explained

| Factor | GDS (Gross Debt Service) | TDS (Total Debt Service) |

|---|---|---|

| Focus | Housing costs only | All debts combined |

| Includes | Mortgage, taxes, heating | Housing + loans + credit cards |

| Limit | Up to 39% | Up to 44% |

| Importance | Primary affordability check | Overall financial risk check |

In simple terms, GDS tells lenders if you can afford your home, while TDS shows whether your overall financial situation is stable.

Other Factors That Affect Mortgage Approval

Debt ratios matter, but they aren’t the only factors lenders review when assessing mortgage applications.

Mortgage Stress Test in Canada

Canada requires borrowers to qualify at a higher interest rate than the one offered by lenders. This rule was introduced by the Office of the Superintendent of Financial Institutions to protect borrowers from rising rates.

As of recent guidelines, borrowers must qualify at the greater of the contract rate plus 2% or the benchmark stress-test rate.

Credit Score Requirements

Most lenders prefer a credit score above 680 for conventional mortgages. Higher scores signal responsible credit management and reduce lending risk.

Down Payment and Mortgage Insurance

Borrowers with smaller down payments must purchase mortgage insurance. According to data from the Financial Consumer Agency of Canada, insured loans follow stricter approval guidelines.

Employment and Income Stability

Lenders typically want to see stable income history, usually two years of consistent employment or self-employment income documentation.

Consistency often matters as much as income level.

How to Improve Your Debt-to-Income Ratio Before Applying

If your ratios are slightly above lender limits, improving them before applying can significantly increase approval chances.

Pay Down High-Interest Debt

Reducing credit card balances can quickly lower your TDS ratio because lenders use minimum payments in their calculations.

Increase Your Down Payment

A larger down payment reduces the mortgage amount, which lowers monthly housing costs and improves both GDS and TDS ratios.

Refinance or Consolidate Debt

Consolidating multiple debts into a single lower payment may improve affordability. For strategies on reducing financial obligations, see this guide on how to lower debt-to-income ratio.

Increase Household Income

Adding a co-borrower or increasing verifiable income can significantly improve ratios and borrowing capacity.

Financial planning tools like the tax toolkit can also help estimate income after taxes when preparing for a mortgage application.

Common DTI Mistakes That Cause Mortgage Rejection

Many mortgage applications fail because borrowers overlook small financial details.

- Opening new credit accounts before closing

- Underestimating property tax and heating costs

- Ignoring credit card minimum payments

- Applying with high revolving debt

A careful review of your finances before applying can prevent these issues.

Expert Tips to Qualify for a Mortgage With Higher DTI

Some borrowers still qualify even with higher ratios when other financial strengths offset the risk.

Pros and Cons of applying with higher debt ratios:

- Pros: potential access to larger mortgage, faster home purchase.

- Cons: higher financial pressure and stricter lender scrutiny.

Mortgage brokers often recommend improving credit score, reducing revolving debt, and securing stable employment before applying.

Industry data from the Canada Mortgage and Housing Corporation shows that borrowers with stronger financial profiles consistently achieve higher approval rates.

Pros and Cons of Mortgage Debt Ratio Rules in Canada

Advantages

- Protects borrowers from over-borrowing

- Ensures long-term financial stability

- Reduces default risk for lenders

- Encourages responsible financial planning

Disadvantages

- Limits borrowing power for high-income earners with debt

- Can delay homeownership for first-time buyers

- Does not always reflect future income growth

- Strict thresholds may reject otherwise capable borrowers

FAQS For DTI for Mortgage Approval Canada

What is the maximum debt-to-income ratio for a mortgage in Canada?

Most Canadian lenders prefer a GDS ratio below 39% and a TDS ratio below 44%. Staying under these thresholds improves your chances of mortgage approval and passing the stress test.

Can you get a mortgage with a high debt-to-income ratio?

It’s possible, but higher ratios increase lending risk. Alternative lenders or co-borrowers may help, and increasing your down payment can offset high debt levels.

What debts are included in the calculation for mortgage approval?

Lenders typically include housing costs, credit card minimum payments, car loans, personal loans, student loans, and lines of credit. Ignoring any of these can lead to an inaccurate debt ratio estimate.

How does student loan debt affect mortgage approval?

Student loans count toward your TDS ratio, even if payments are deferred. Lenders usually include the required monthly payment when calculating affordability.

How can I lower my debt-to-income ratio before applying?

You can lower your ratio by paying down high-interest debt, consolidating loans, increasing your down payment, or adding a co-borrower. Using a debt-to-income calculator can help you track improvements efficiently.

What is the difference between GDS and TDS ratios?

GDS measures the portion of income used for housing costs only, while TDS includes all debts. Both ratios are used together to evaluate mortgage affordability in Canada.

Do mortgage stress tests affect debt-to-income requirements?

Yes. Stress tests require borrowers to qualify at a higher interest rate than their mortgage rate, effectively lowering the affordable mortgage amount and impacting both GDS and TDS ratios.

Ready to Improve Your Mortgage Approval Chances?

Before applying, take time to calculate your GDS and TDS ratios accurately. Even small adjustments — like paying down a credit card or increasing your down payment — can make a major difference.

Pro tip: Review your financial profile 3–6 months before applying. This gives you enough time to optimize your ratios and strengthen your application.

Quick Summary

Understanding dti for mortgage approval canada helps buyers estimate their borrowing capacity before applying. Canadian lenders rely primarily on GDS and TDS ratios, with common limits around 39% and 44% respectively.

Maintaining manageable debt levels, stable income, and strong credit can significantly improve mortgage approval chances. By calculating your ratios early and adjusting your finances where necessary, you can approach lenders with confidence and a stronger mortgage application.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is the maximum debt-to-income ratio for a mortgage in Canada?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Most Canadian lenders prefer a GDS ratio below 39% and a TDS ratio below 44%. Staying under these thresholds improves your chances of mortgage approval and passing the stress test.” } }, { “@type”: “Question”, “name”: “Can you get a mortgage with a high debt-to-income ratio?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “It’s possible, but higher ratios increase lending risk. Alternative lenders or co-borrowers may help, and increasing your down payment can offset high debt levels.” } }, { “@type”: “Question”, “name”: “What debts are included in the calculation for mortgage approval?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Lenders typically include housing costs, credit card minimum payments, car loans, personal loans, student loans, and lines of credit. Ignoring any of these can lead to an inaccurate debt ratio estimate.” } }, { “@type”: “Question”, “name”: “How does student loan debt affect mortgage approval?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Student loans count toward your TDS ratio, even if payments are deferred. Lenders usually include the required monthly payment when calculating affordability.” } }, { “@type”: “Question”, “name”: “How can I lower my debt-to-income ratio before applying?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “You can lower your ratio by paying down high-interest debt, consolidating loans, increasing your down payment, or adding a co-borrower. Using a debt-to-income calculator can help you track improvements efficiently.” } }, { “@type”: “Question”, “name”: “What is the difference between GDS and TDS ratios?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “GDS measures the portion of income used for housing costs only, while TDS includes all debts. Both ratios are used together to evaluate mortgage affordability in Canada.” } }, { “@type”: “Question”, “name”: “Do mortgage stress tests affect debt-to-income requirements?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes. Stress tests require borrowers to qualify at a higher interest rate than their mortgage rate, effectively lowering the affordable mortgage amount and impacting both GDS and TDS ratios.” } } ] }