A driver in Toronto comparing vehicles might notice something confusing. A brand-new sedan may offer a lower interest rate, yet the price is much higher than a similar used car. That’s where a new vs used car loan comparison becomes important. The right financing choice can change the total cost of owning a vehicle by thousands of dollars.

This guide explains how car loans work in Canada, how interest rates differ between new and used vehicles, and when each option actually saves money. You’ll also see real financing examples, cost comparisons, and practical tips to help you choose the smarter auto loan.

Table of Contents

New vs Used Car Loan Comparison Which Financing Option Is Cheaper in Canada?

Choosing between a new and used vehicle often comes down to financing. Lenders treat each option differently because the risk, resale value, and depreciation vary. A proper comparison helps you understand not just the monthly payment, but the total cost of the loan over time.

Understanding How Car Loans Work in Canada

Before comparing new and used loans, it helps to understand how auto financing works. A car loan spreads the cost of a vehicle over several years while adding interest charged by the lender.

Most Canadian lenders — including major banks, dealerships, and credit unions — structure auto loans using fixed interest rates and monthly payments.

What Is an Auto Loan?

An auto loan is a type of installment loan used to purchase a vehicle. The lender pays the dealership upfront, and the borrower repays the balance over a set term with interest.

Typical loan terms in Canada range from 36 to 84 months. According to industry data referenced by Bank of Canada economic reports, auto financing is one of the most common forms of consumer credit nationwide.

Key Components of a Car Loan

Several factors determine how much a car loan will cost:

- Loan amount (vehicle price minus down payment)

- Interest rate offered by the lender

- Loan term length

- Borrower credit score

- Vehicle type and age

Even small differences in interest rate or term can significantly affect the final cost.

How Monthly Car Payments Are Calculated

Auto loans use amortization. Each payment covers part of the principal and part of the interest. Early payments mostly pay interest, while later payments reduce the loan balance faster.

If you’d like to test real numbers, this short calculator example shows how changing rates or loan terms affects payments.

Calculate Your Auto Loan Payment

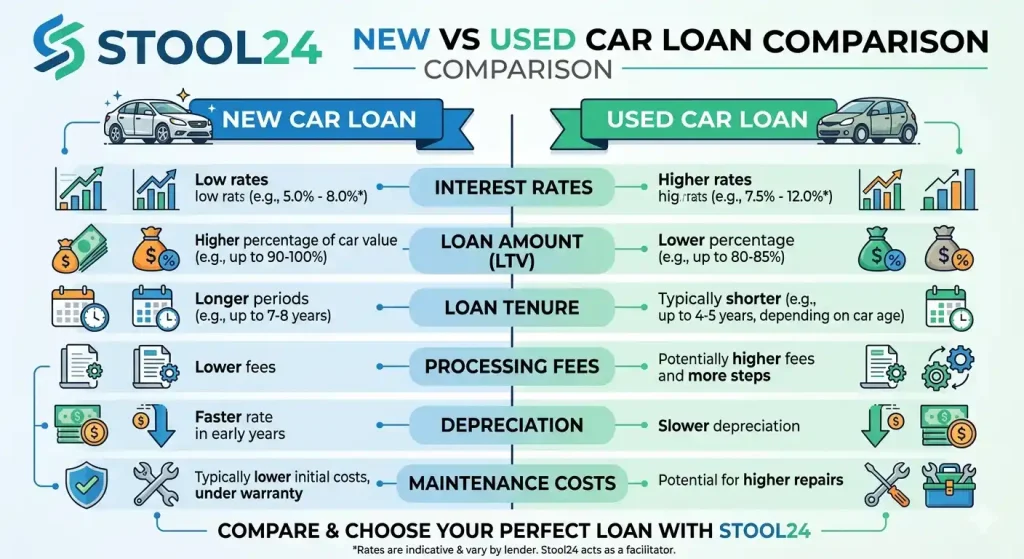

New vs Used Car Loan Comparison

The biggest differences between financing new and used vehicles involve interest rates, loan terms, and depreciation risk. Lenders see older vehicles as slightly riskier, which usually leads to higher rates.

The table below shows the key differences between both financing options.

| New vs Used Car Loan Comparison Factors | New Car Loan | Used Car Loan |

|---|---|---|

| Average Interest Rate | Lower | Higher |

| Vehicle Price | Higher | Lower |

| Loan Terms | Up to 84 months | Often shorter |

| Depreciation | Fast early depreciation | Slower depreciation |

| Warranty Coverage | Full manufacturer warranty | Limited or expired |

For a deeper breakdown of financing costs and rate trends, you can also explore detailed analysis in the Canadian car loan interest rate guide.

Average Car Loan Rates in Canada

Interest rates vary depending on credit score and lender type. Dealership promotions sometimes offer lower rates for new vehicles, especially when manufacturers subsidize financing.

The following table illustrates typical ranges.

| Average Auto Loan Rates by Credit Score in Canada | New Car Rate | Used Car Rate |

|---|---|---|

| Excellent (750+) | 5–7% | 6–8% |

| Good (700–749) | 6–8% | 7–9% |

| Fair (650–699) | 7–9% | 8–11% |

Industry research referenced by the Canadian Bankers Association indicates that new vehicle financing typically carries slightly lower risk for lenders because resale value is easier to predict.

Loan Term Differences

New car loans often allow longer terms — sometimes up to 84 months. Used vehicle financing is frequently capped at shorter terms depending on the vehicle’s age.

Longer terms lower the monthly payment but increase the total interest paid.

That trade-off matters more than most buyers realize.

A vehicle financed over 84 months may still be worth less than the remaining loan balance during the early years.

Total Cost Example: New vs Used Car Loan

Looking only at monthly payments can be misleading. The true comparison comes from analyzing purchase price, interest, and depreciation together.

Example Scenario: Financing a New Car

Suppose a buyer finances a new car priced at $38,000 with a 6.5% interest rate over 72 months.

- Loan amount: $38,000

- Monthly payment: about $640

- Total interest paid: about $8,100

The biggest hidden cost is depreciation. According to data referenced by AutoTrader Canada market insights, new vehicles can lose 15–20% of their value in the first year alone.

Example Scenario: Financing a Used Car

Now consider a three-year-old vehicle priced at $26,000 financed at 8% for 60 months.

- Loan amount: $26,000

- Monthly payment: about $525

- Total interest paid: about $5,500

Even with the higher rate, the lower purchase price significantly reduces total borrowing costs.

The table below summarizes the difference.

| Total Cost Comparison Example | New Car | Used Car |

|---|---|---|

| Purchase Price | $38,000 | $26,000 |

| Total Interest | $8,100 | $5,500 |

| Estimated Depreciation (3 yrs) | $12,000 | $6,000 |

Pros and Cons of Financing New vs Used Cars

Each option has financial advantages depending on your priorities.

Pros and Cons of New Car Financing

- Pros: lower interest rates, full warranty, latest technology

- Cons: higher purchase price, rapid depreciation, larger loan

Pros and Cons of Used Car Financing

- Pros: lower purchase price, slower depreciation, smaller loan balance

- Cons: higher interest rates, limited warranty, possible maintenance costs

Many Canadian buyers choose lightly used vehicles because they balance price and reliability.

When Financing a New Car Makes More Sense

In some situations, new car financing actually becomes the better deal.

Manufacturer Incentives

Automakers occasionally offer promotional financing such as 0% or very low rates. These incentives can reduce interest costs dramatically.

Long-Term Ownership

If you plan to keep a car for 8–10 years, depreciation becomes less important. The vehicle will likely be driven until its value is minimal.

Warranty and Maintenance

New vehicles include full manufacturer warranties, which may reduce repair costs during the early ownership period.

When a Used Car Loan Is the Better Choice

Used car financing often works best for buyers who prioritize lower borrowing costs.

Lower Overall Loan Balance

A smaller loan means less interest paid over time, even if the rate is slightly higher.

Avoiding Early Depreciation

The steepest value drop happens in the first few years of ownership. Buying used allows someone else to absorb that loss.

Shorter Loan Terms

Used vehicles are frequently financed over shorter periods, which helps borrowers become debt-free faster.

Expert Tips to Choose the Best Car Loan

Small financial decisions can significantly reduce the cost of a car loan.

- Compare dealership financing with bank or credit union loans

- Increase your down payment when possible

- Choose the shortest loan term you can comfortably afford

- Improve your credit score before applying

Financial planning tools can also help evaluate different borrowing scenarios.

Many Canadians also compare other financial calculators and tax resources available in the Tax Toolkit financial resource hub, which compiles various budgeting and financial planning tools.

Common Car Loan Mistakes Buyers Make

Even experienced buyers occasionally focus on the wrong factors when financing a vehicle.

Focusing Only on Monthly Payment

A lower monthly payment may simply mean a longer loan term and more interest paid overall.

Choosing Very Long Loan Terms

Loans lasting 84 months increase the risk of negative equity if the vehicle depreciates faster than the loan balance.

Ignoring Depreciation

The biggest financial loss with vehicles often comes from depreciation rather than loan interest.

FAQS For New vs Used Car Loan Comparison

Is it cheaper to finance a new or used car in Canada?

It depends on the purchase price and interest rate. New cars usually have lower loan rates, but their higher prices often increase the total loan amount. In many cases, a used vehicle still costs less overall because the loan balance and depreciation are smaller.

Why are used car loan interest rates higher than new car rates?

Lenders see used vehicles as slightly riskier because older cars may lose value faster and have more mechanical uncertainty. To offset that risk, financial institutions usually charge higher interest rates. The exact rate depends on factors such as credit score, vehicle age, and lender policies.

What is the average car loan interest rate in Canada?

Average auto loan rates in Canada generally range from about 5% to 9% for borrowers with good credit. New vehicles often qualify for lower promotional rates, while used car loans tend to fall on the higher end of the range. Rates can vary depending on credit history, loan term, and the lender.

Should I choose a longer car loan term to reduce monthly payments?

A longer loan term can lower the monthly payment, but it usually increases the total interest paid. Many financial experts recommend choosing the shortest term that fits comfortably within your budget. This reduces the overall borrowing cost and helps you build equity in the vehicle faster.

How much down payment is recommended for a car loan?

Many lenders suggest putting down at least 10% to 20% of the vehicle price. A larger down payment lowers the loan amount and reduces monthly payments. It also helps avoid negative equity if the vehicle depreciates quickly.

Is dealership financing better than bank auto loans in Canada?

Dealership financing can offer competitive promotional rates, especially on new vehicles. However, banks and credit unions sometimes provide better terms depending on your credit profile. Comparing both options before signing a loan agreement helps ensure you get the best rate.

Does credit score affect new vs used car loan approval?

Yes, credit score plays a major role in auto loan approval and interest rates. Borrowers with higher scores usually qualify for lower rates and better loan terms. Improving your credit score before applying can significantly reduce the total cost of financing.

Quick Summary

A proper new vs used car loan comparison helps buyers understand the real financial impact of each option. New vehicles typically offer lower interest rates and warranties, but higher prices and faster depreciation. Used cars usually carry higher rates yet cost less overall because the purchase price is lower.

The best choice depends on budget, loan terms, and how long you plan to keep the vehicle. By comparing interest rates, depreciation, and total loan costs before buying, Canadian drivers can avoid expensive financing mistakes and make a smarter auto purchase.